- Article Category

- IRS Form 5471

Updated Posted

Installment 2. Is the Foreign Corporation a “Foreign-Controlled CFC”?

Phil Hodgen

Attorney, Principal

Share

Hello and welcome to the second installment in the series that will explain, in gruesome and tedious detail, how to figure out the Category 5 filing requirements.

The Series

Completed installment:

- Installment 1: Why? And Your Checklist. If you understand how the IRS tried to fix what Congress broke, the whole exercise of figuring out which (sub)category applies will be a bit easier.

This installment:

- Installment 2: Foreign-Controlled CFCs. Is your foreign corporation a “foreign-controlled CFC” or a “U.S.-controlled CFC” and why does this matter? (Hint: U.S.-controlled CFCs go straight to Category 5a.)

Future installments:

- Installment 3: Related or Unrelated? Is your United States shareholder “related” or “unrelated” to the foreign-controlled controlled CFC?

- Installment 4: What Kind of Shareholder? Is your United States shareholder a “section 958(a) U.S. shareholder” or a “constructive U.S. shareholder”?

- Installment 5: Checking the Right Box. We pull it all together. You will know whether your United States shareholder is a Category 5a, 5b, or 5c filer, or maybe you hit the jackpot—and the Category 5 filing requirement is waived entirely.

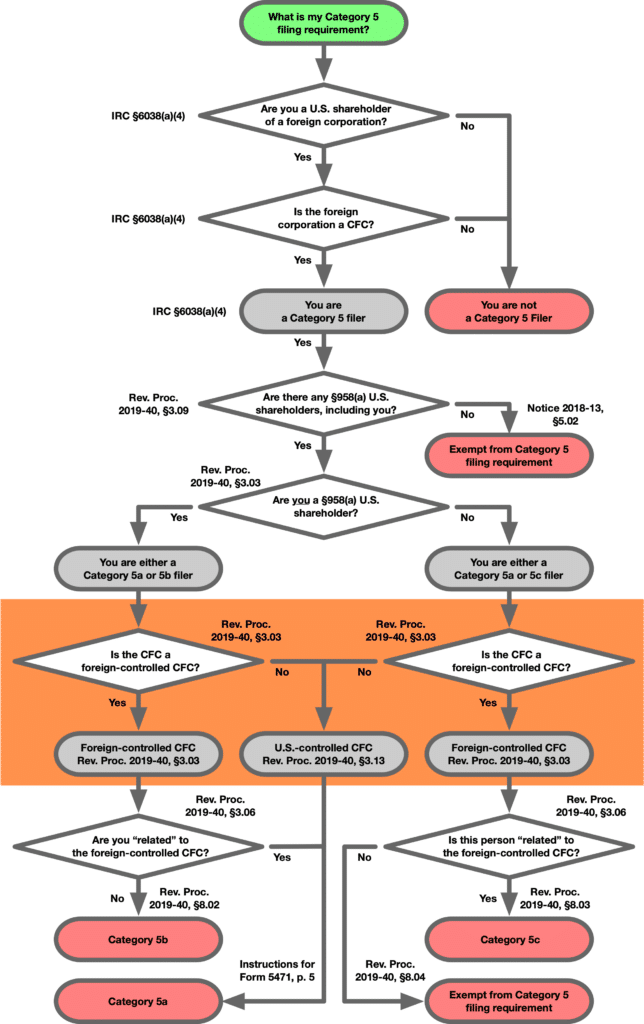

The Category 5 flowchart

Because I know you love flowcharts, here is a flowchart you can use to determine whether your particular situation calls for Category 5a, 5b, or 5c filing — or if you are lucky, an exception allows to you to not file as a Category 5 filer at all.

The topic for this week’s newsletter is highlighted in orange: Is this foreign corporation a “foreign-controlled CFC” or its inverse, a “U.S.-controlled CFC?”

Why you have to figure out "foreign-controlled" or "U.S.-controlled"

Downward attribution rules can create controlled foreign corporations in unexpected ways. This creates situations where U.S. taxpayers are required to provide information that they cannot, as a practical matter, obtain. How, then, can they prepare and file Form 5471?

Rev. Proc. 2019-40 recognized this "lack of information" problem. It identified two factors that affect whether a U.S. taxpayer can--as a practical matter--get the data needed to fully complete Form 5471:

- “Foreign-controlled.” If foreign shareholders are in control of the foreign corporation, a U.S. shareholder is less likely to be able to get financial data from the foreign corporation.

- “Related vs. unrelated.” Some informal relationships are better than others. If you are “unrelated” to the source of data you are less likely to get voluntary cooperation.

This week, I cover the “foreign-controlled” question. Next time I will deal with the “related” or “unrelated” question.

"Foreign-controlled CFC" defined

The definition comes from Rev. Proc. 2019-40, Section 3.03:

The term "foreign-controlled CFC" means a foreign corporation that is a CFC but that would not be a CFC, if the determination were made without applying subparagraphs (A), (B), and (C) of section 318(a)(3) so as to consider a U.S. person as owning stock which is owned by a foreign person.

This requires determining controlled foreign corporation status with and without downward attribution from a foreign person. If the answer "with" is different from the answer "without" downward attribution from a foreign person to a U.S. person, then you have a foreign-controlled CFC:

- It's a "CFC" because using today's law (with downward attribution from a foreign person to a U.S. person) it's a CFC.

- It's "foreign-controlled" because the attribution from a foreign person to a U.S. person is what caused the CFC status.

How to figure out if this is a "foreign-controlled CFC"

First, let me give you a quick explanation of what Rev. Proc. 2019-40 wants you to do. Then I will give you an example to walk through.

Simple explanation

Here's what you do:

- Figure out if the foreign corporation is a controlled foreign corporation. Use today's law, as-is.

- Figure out if the foreign corporation is a controlled foreign corporation. Use the pre-TCJA law, pretending that IRC §958(b)(4) still existed.

- If the answer to #1 is "yes, it's a CFC" and the answer to #2 is "no, it's not a CFC," then you have a foreign-controlled CFC.

The process is explained in tedious detail below.

Step 1. Is this a CFC, using downward attribution from foreign persons?

A controlled foreign corporation is a foreign corporation that is more than 50% owned by United States shareholders. IRC §957(a). You figure out who the United States shareholders are by using the stock ownership rules of IRC §958(a) and IRC §958(b). IRC §951(b).

The first step is to simply apply the rules as-is. After all, you are preparing today's income tax return, so you apply the tax rules as they are today.

- Identify the United States persons who own stock in a foreign corporation.

- Figure out how much stock each U.S. person own, using the stock ownership rules of IRC §958(a) and IRC §958(b). Important: IRC §958(b) applies the downward attribution rules of IRC §318(a)(3), and IRC §318(a)(3) allows downward attribution from anyone--a U.S. person or a foreign person.

- For every U.S. person who owns stock in the foreign corporation, take the ones who own 10% or more. Add their ownership percentages together.

- If the combined value is greater than 50%, the foreign corporation is a controlled foreign corporation.

If you have decided that you have a controlled foreign corporation, each United States person who owns 10% or more of the stock (a "United States shareholder" as defined in IRC §951(b)) has a Category 5 problem.

Step 2. Is this a CFC, WITHOUT downward attribution from foreign persons?

Now, do your work again. Determine whether the corporation is a controlled foreign corporation, but this time do not interpret IRC §318(a)(3) in such a way as to attribute foreign corporation stock from a foreign person to a domestic entity that the foreign person owns.

In other words, do exactly what you would have done in 2017, before repeal of IRC §958(b)(4).

Rev. Proc. 2019-40, Section 3.03 tells you to do this:

The term "foreign-controlled CFC" means a foreign corporation that . . . would not be a CFC, if the determination were made without applying subparagraphs (A), (B), and (C) of section 318(a)(3) so as to consider a U.S. person as owning stock which is owned by a foreign person.

In other words, identifying United States shareholders and calculating their stock ownership is done in the same way as always, except for the downward attribution rules, which are in IRC §318(a)(3):

- Yes, apply the downward attribution rules to determine stock ownership if the attribution is from a U.S. person to a U.S. person.

- No, do not apply the downward attribution rules to determine stock ownership if the attribution is from a foreign person to a U.S. person.

Nota bene. IRC §318(a)(3) deals with attribution from anyone to a "U.S. person" that is a partnership (IRC §318(a)(3)(A)), estate (IRC §318(a)(3)(A)), trust (IRC §318(a)(3)(B)), or corporation (IRC §318(a)(3)(C)).

Therefore, the downward attribution rules can never be used to attribute stock to a U.S. human being taxpayer.

Step 3. Pull it all together

Now you have determined (in Step 1) whether the foreign corporation in question is a controlled foreign corporation. Or not!

Compare the Step 1 and Step 2. A foreign-controlled CFC exists if:

- Step 1 is "yes" (this is definitely a CFC), and

- Step 2 is "no" (which means that the thing that pushed the corporation over the edge to CFC status is downward attribution from a foreign person).

| CFC with downward attribution from foreign persons | CFC without downward attribution from foreign persons | Foreign-controlled or U.S.-controlled CFC? |

|---|---|---|

| Yes | Yes | U.S.-controlled |

| Yes | No | Foreign-controlled |

| No | Yes | Impossible |

| No | No | Not a CFC |

Example

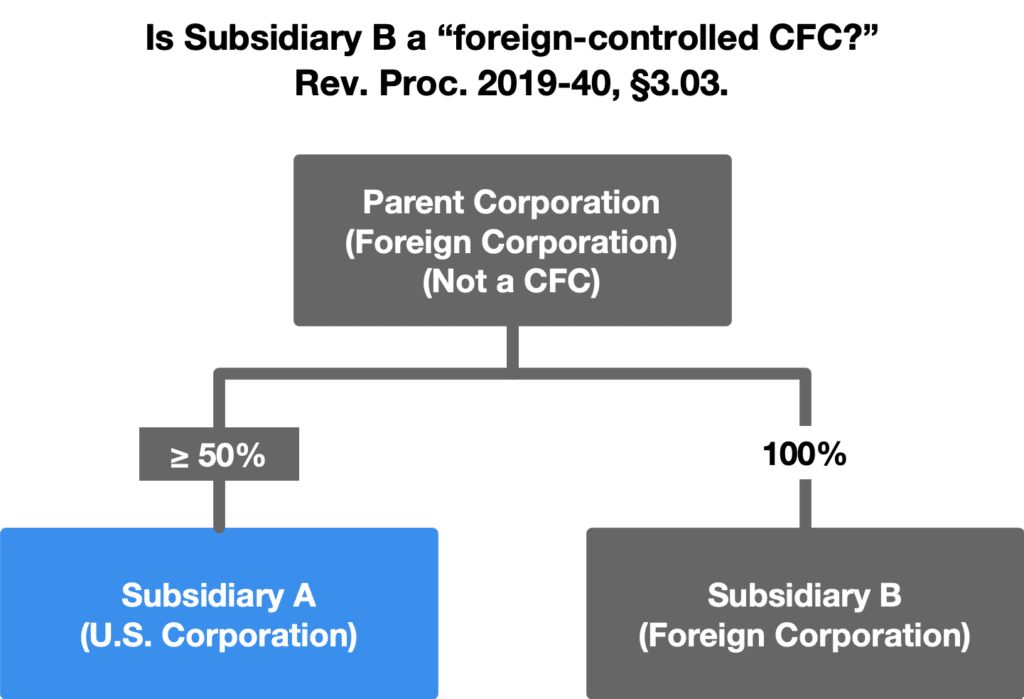

Let’s walk through an example to see how the definition of a foreign-controlled controlled foreign corporation works. This shows the sequence that I follow in doing a project like this.

The questions, in sequence

We want to know three things:

- Is Subsidiary A a “United States shareholder” of Subsidiary B?

- Is Subsidiary B a “controlled foreign corporation" with IRC §958(a) and IRC §958(b) applied as-is?

- Is Subsidiary B a “controlled foreign corporation" with IRC §958(a) and IRC §958(b) applied without downward attribution from a foreign person?

I do the United States shareholder analysis first, because you can't figure out whether a foreign corporation is a CFC until you have identified all of the United States shareholders.

Subsidiary A is a United States shareholder

A United States shareholder is a United States person who owns (as defined by IRC §§958(a) and 958(b)) 10% or more of the stock of a foreign corporation. IRC §951(b).

Subsidiary A is considered to be the constructive owner of 100% of the stock of Subsidiary B within the definition of IRC §958(b). Here's why.

We are told by IRC §958(b) to use the rules of IRC §318(a) to determine constructive ownership. There are three modifications to the IRC §318(a) rules given by IRC §958(b)(1)-(3) but none of them matter to this example.

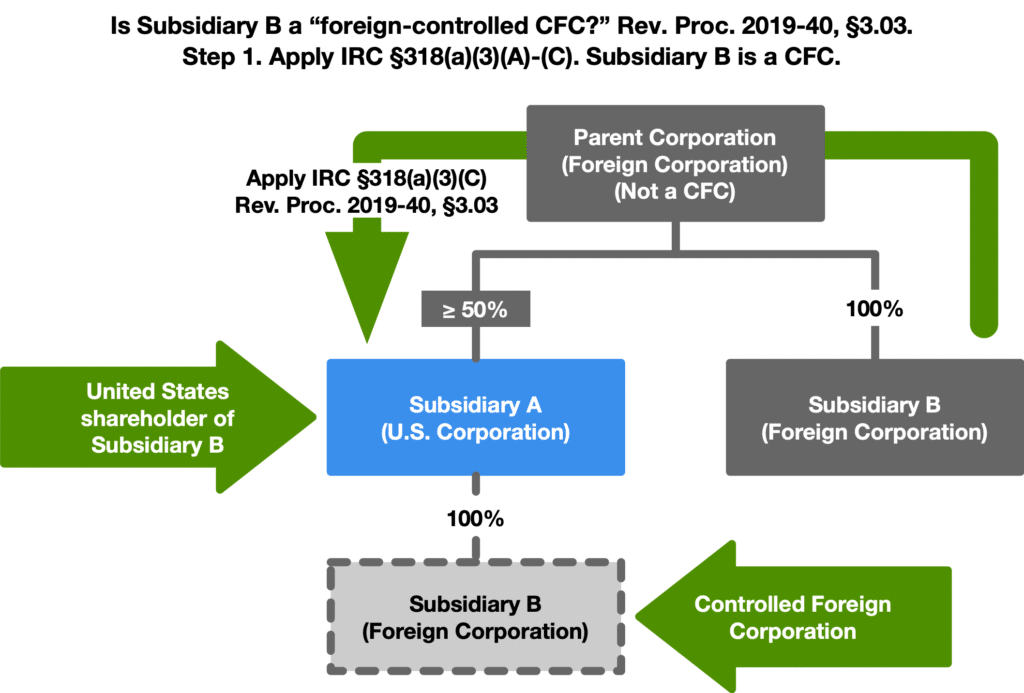

IRC §318(a)(3)(C) gives the downward attribution rule: a corporation owns stock owned by its shareholders:

“If 50 percent or more in value of the stock in a corporation is owned, directly or indirectly, by or for any person, such person shall be considered as owning the stock owned, directly or indirectly, by or for such corporation, in that proportion which the value of the stock which such person so owns bears to the value of all the stock in such corporation.”

We apply IRC §318(a)(3)(C) as-is: downward attribution from foreign persons is permitted.

In this example, Foreign Parent is assumed to own 50% or more of Subsidiary A. Therefore, Subsidiary A is considered as owning all of the Subsidiary B stock that is directly owned by Foreign Parent.

Conclusion: Subsidiary A is the constructive shareholder of 100% of the stock of Subsidiary B. Therefore, Subsidiary A is a United States shareholder of Subsidiary B because it owns at least 10% of Subsidiary B’s stock.

Subsidiary B is a CFC when you apply the downward attribution rules

Now we have to figure out whether Subsidiary B is a controlled foreign corporation.

A foreign corporation is a controlled foreign corporation when more than 50% of its stock (by vote or value) is owned by United States shareholders. IRC §957(a).

We just figured out that 100% of the stock of Subsidiary B is considered to be owned by Subsidiary A, which is a United States shareholder.

Therefore, Subsidiary B is a controlled foreign corporation.

That's the first prong of the test in Rev. Proc. 2019-40, Section 3.03: CFC status under a default/normal analysis using today's law.

Subsidiary B is not a CFC when you omit downward attribution from a foreign person

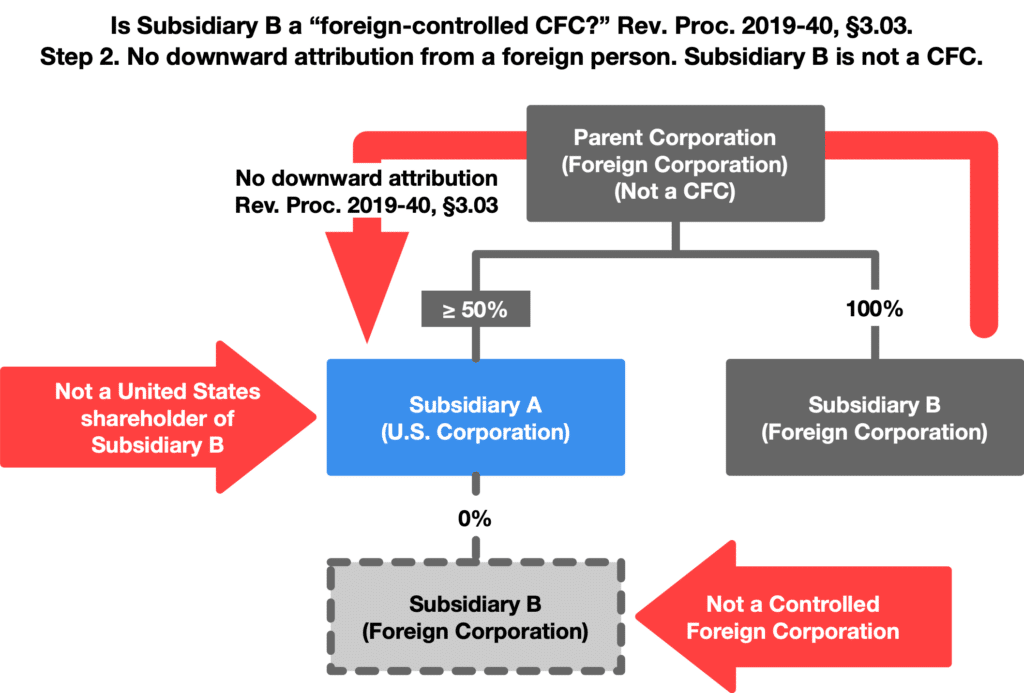

A “foreign-controlled CFC” is a foreign corporation that is a CFC when you apply the downward attribution rules and is not a CFC when you ignore the downward attribution rules. Just to make it easy to follow the discussion, I reference Rev. Proc. 2019-40, §3.03 yet again (emphasis added):

The term "foreign-controlled CFC" means a foreign corporation that is a CFC but that would not be a CFC, if the determination were made without applying subparagraphs (A), (B), and (C) of section 318(a)(3) so as to consider a U.S. person as owning stock which is owned by a foreign person.

The second leg of the determination of whether Subsidiary B is a foreign-controlled CFC is for you to do the work all over again, but this time omit the application of the downward attribution rules of IRC §318(a)(3)(A)-(C).

If this analysis says Subsidiary B is still a CFC, then Subsidiary B is not a foreign-controlled foreign corporation.

There is no possible way (except for the downward attribution rules, which we are ignoring) for Subsidiary A to be considered a shareholder of Subsidiary B:

- IRC §958(a)(1) is impossible: Subsidiary A does not directly own Subsidiary B stock.

- IRC §958(a)(2) is impossible: Subsidiary A does not indirectly own Subsidiary B stock through a foreign entity.

- IRC §958(b) is impossible because neither IRC §318(a)(1) [family attribution] nor IRC §318(a)(2) [upward attribution] cause Subsidiary A to be treated as owning Subsidiary B stock.

Since Subsidiary A cannot be considered to be a shareholder of Subsidiary B, there is no possibility for Subsidiary B to be a controlled foreign corporation. It has no U.S. shareholders.

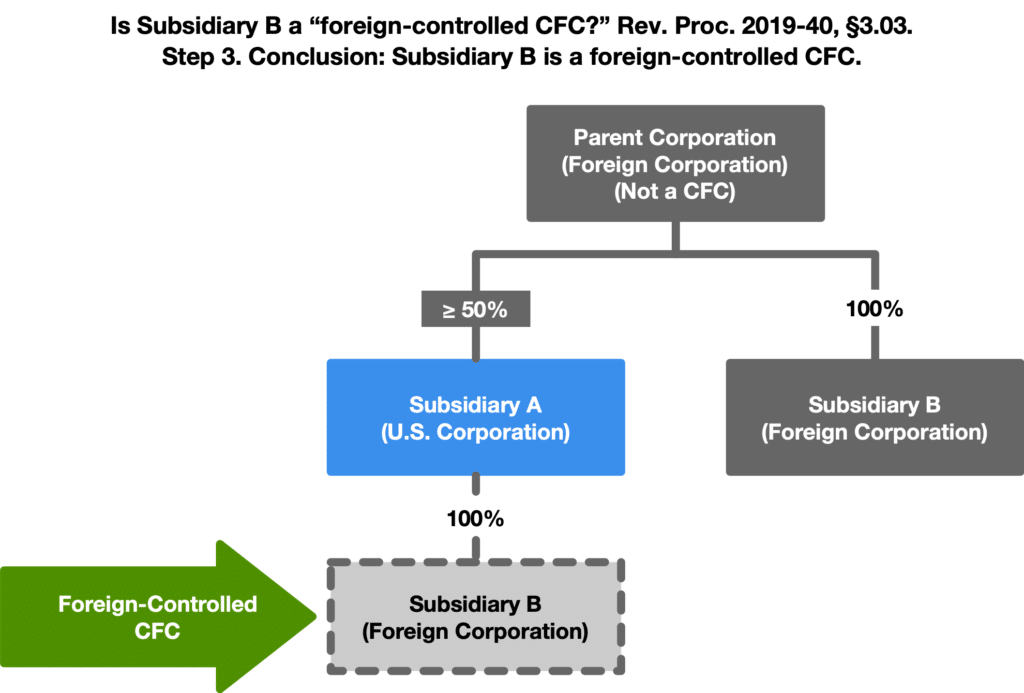

Conclusion: Subsidiary B is a foreign-controlled CFC

Subsidiary B is a controlled foreign corporation if you take into account the downward attribution rules, and Subsidiary A is a United States shareholder.

Subsidiary A has a Category 5 Form 5471 filing requirement.

What kind of Category 5 filing requirement? That is still to be determined, by parsing the rules of Rev. Proc. 2019-40 to determine whether Subsidiary A is a Category 5a, 5b, or 5c filer.

But because the attribution results without downward attribution yielded a “not a CFC” result, Subsidiary B is a foreign-controlled CFC.

Next time . . . Is Subsidiary A “related” to Subsidiary B?

So far we know that Rev. Proc. 2019-40, §3.03 characterizes Subsidiary B as a foreign-controlled CFC. In the next installment we look at another factor that you must figure out in order to put Subsidiary A in the Category 5a, 5b, or 5c filing bucket: "related" or "unrelated" status.

Aside. Isn't it interesting how over any considerable period of time any particular change to tax law makes things worse, never better?

Stay tuned for the next exciting episodes of this Category 5 filer series, where I explore the next factor that will tell you which box to check in Item B:

- Is Subsidiary A “related” to Subsidiary B?