- Article Category

- IRS Form 5471

- Published on

Demystify Category 5 Installment 4: Is the U.S. Shareholder Related or Unrelated?

Phil Hodgen

Attorney, Principal

Share

Hello and welcome to Installment 4 of a 5 part series to help you figure out whether a U.S. shareholder is a Category 5a, 5b, or 5c filer of Form 5471.

The series so far

Completed installments:

- Installment 1: Why? And Your Checklist. If you understand how the IRS tried to fix what Congress broke, the whole exercise of figuring out which (sub)category applies will be a bit easier.

- Installment 2: Foreign-Controlled CFCs. Is your foreign corporation a “foreign-controlled CFC” or a “U.S.-controlled CFC” and why does this matter? (Hint: U.S.-controlled CFCs go straight to Category 5a.)

- Installment 3: What Kind of Shareholder? Is your United States shareholder a “section 958(a) U.S. shareholder” or a “constructive U.S. shareholder”?

This installment:

- Installment 4: Related or Unrelated? Is your United States shareholder “related” or “unrelated” to the foreign-controlled controlled CFC?

Future installments:

- Installment 5: Checking the Right Box. We pull it all together. You will know whether your United States shareholder is a Category 5a, 5b, or 5c filer, or maybe you hit the jackpot—and the Category 5 filing requirement is waived entirely.

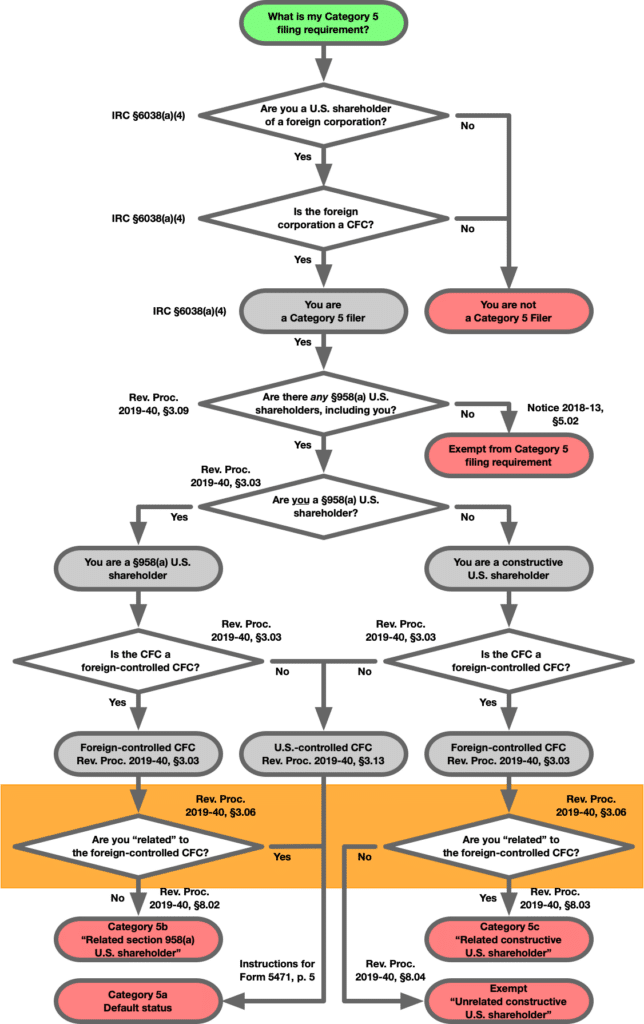

The Category 5 flowchart

Here is the handy-dandy flowchart for figuring out the answers to your Category 5 dilemmas. This week’s topic is highlighted in garish orange.

History of the Category 5 problem we’re solving

The problem we’re solving is “which Category 5 box do I check?”

Congress caused the problem by its repeal of IRC §958(b)(4) in 2017.

The repeal of IRC §958(b)(4) created new Category 5 filers who legitimately have little or no access to the information they need to complete Form 5471.

It created a group of people who couldn’t even tell if they were Category 5 filers or not.

The IRS fixed the problem in Rev. Proc. 2019-40.

The IRS fixed the politician-created problem by making tax return preparation more complicated. Instead of Category 5, we now have Categories 5a, 5b, and 5c and a complicated system to figure it all out.

Ye olden tymes: “Category 5 filer is . . .”

. . . a United States shareholder of a controlled foreign corporation. IRC §6038(a)(4).

Nowadays: “Category 5a/5b/5c filer is . . .”

Determining the right Category 5 box to check is a game of Mad Libs. IRC §6038(a)(4) plus Rev. Proc. 2019-40.

. . . a [__] [_] United States shareholder of a [___] controlled foreign corporation.

Rev. Proc. 2019-40 added some adjectives to make the filing obligations calibrated to the taxpayer’s ability to get access to data from/about the foreign corporation.

- What type of U.S. shareholder?

- Type of stock ownership: determined under IRC §958(a) and IRC §958(b), or determined under IRC §958(b) only.

- Related party or unrelated party to the foreign corporation.

- What type of CFC?

- Control by U.S. shareholders caused by downward attribution (”foreign-controlled”) or control by U.S. shareholders exists without downward attribution?

So the Mad Libs game looks like this. I have highlighted this week’s topic.

. . . a [TYPE OF STOCK OWNERSHIP] [RELATED PARTY STATUS] United States shareholder of a [CONTROLLING STOCK CAUSED BY DOWNWARD ATTRIBUTION] controlled foreign corporation.

Key insight: the IRS recycled the “related party” idea

The idea of “related party” rules in the Code is everywhere. The government expects conspiracies and skullduggery among related parties — to the detriment of Uncle Sam’s wallet.

In Rev. Proc. 2019-40, the IRS uses a definition of “related party” that already exists in the Subpart F rules and extends it to define and refine a shareholder’s Category 5 reporting requirements.

For Form 5471 filing purposes, if you are “related” you are expected, in real life, to have enough clout to get information you need from the foreign corporation. If you are unrelated, you may not have the ability to get data needed for Form 5471 preparation.

“Related person” for Category 5 purposes

Rev. Proc. 2019-40’s magnificently awkward definition

Rev. Proc. 2019-40, Section 3.06 recycles another part of the Code to define a “related person” for Category 5 purposes.

The term "related person" means, with respect to a person, another person described in section 954(d)(3), substituting the first-mentioned person for "controlled foreign corporation" each place it appears.

Magnificently awkward prose.

What they meant to say is “look at the U.S. shareholder and see if it is related to the foreign corporation, and use IRC §954(d)(3) to figure it out.”

U.S. shareholder ← (”related”) → foreign corporation

We can tell that Rev. Proc. 2019-40 wants to examine the relationship between the U.S. shareholder (for whom we are trying to puzzle through the Category 5 conundrum) and the foreign corporation.

This is demonstrated is the definition of “related” constructive U.S. shareholders. Rev. Proc. 2019-40, Section 3.05 says (emphasis added):

The term "related constructive U.S. shareholder" means, with respect to a foreign corporation, a constructive U.S. shareholder that is a related person with respect to the foreign corporation.

“Related” is found where there is control

Whether the U.S. shareholder (the one with a Form 5471 problem) is “related” to the foreign corporation depends on the definition in IRC §954(d)(3).

Related person defined. For purposes of this section, a person is a related person with respect to a controlled foreign corporation, if—

- (A) such person is an individual, corporation, partnership, trust, or estate which controls, or is controlled by, the controlled foreign corporation, or

- (B) such person is a corporation, partnership, trust, or estate which is controlled by the same person or persons which control the controlled foreign corporation.

There are three kinds of control:

- The U.S. shareholder controls the foreign corporation. IRC §954(d)(3)(A).

- The foreign corporation controls the U.S. shareholder. IRC §954(d)(3)(A).

- A common owner controls both the foreign corporation and the U.S. shareholder. IRC §954(d)(3)(B).

“Control” means more than 50% ownership of stock

The flush language of IRC §954(d)(3) defines “control” as the usual “more than 50% of the stock by vote or value.”

For purposes of the preceding sentence, control means, with respect to a corporation, the ownership, directly or indirectly, of stock possessing more than 50 percent of the total voting power of all classes of stock entitled to vote or of the total value of stock of such corporation. In the case of a partnership, trust, or estate, control means the ownership, directly or indirectly, of more than 50 percent (by value) of the beneficial interests in such partnership, trust, or estate. For purposes of this paragraph, rules similar to the rules of section 958 shall apply.

“Ownership” has its own special definition (sigh)

Control means ownership “directly or indirectly” of stock. This phrase is defined in the Regs. §1.954-1(f)(2)(iv). Two important rules apply:

- For direct and indirect ownership of stock (as defined by IRC §958(a)), it doesn’t matter whether an entity is foreign or domestic. Reg. §1.954-1(f)(2)(iv)(A).

- For constructive ownership of stock (as defined by IRC §958(b)), the downward attribution rules do not apply. Reg. §1.954-1(f)(2)(iv)(B)(1).

Example

Here is a simple example where a U.S. subsidiary is a Category 5 filer through downward attribution. The U.S. subsidiary is also a related party to the foreign corporation.

Checklist for Rev. Proc. 2019-40 “Related” Status

Here is your step-by-step action checklist for determining whether your U.S. shareholder is “related” or “unrelated” to the foreign corporation, as those terms are defined in Rev. Proc. 2019-40.

Authority

Here is the authority you need to do the job:

- Rev. Proc. 2019-40, §3.06 — definition of “related person.” Tells you to use IRC §954(d)(3) for this job.

- IRC §954(d)(3) — definition of “related person.”

- Reg. §1.954-1(f)(1) — definition of “related person.”

- Reg. §1.954-1(f)(2) — definition of “control,” and specifically what ownership of stock means and the special rules used to determine ownership for related person purposes.

Checklist

- Check for IRC §954(d)(3)(A) related party status.

- From your previous analysis (where you computed the stock ownership that your U.S. shareholder has in the foreign corporation), you computed the U.S. shareholder’s total stock ownership percentage in the foreign corporation: direct, indirect, and constructive ownership as defined in IRC §958(a) and IRC §958(b).

- If the percentage is more than 50%, stop. You have your answer: your U.S. shareholder is a related party to the foreign corporation.

- IRC §954(d)(3)(A) says a U.S. shareholder is a related party to a foreign corporation if the U.S. shareholder controls the foreign corporation.

- IRC §954(d)(3) says “control” means ownership of more than 50% of the foreign corporation’s stock, by vote or value.

- Your U.S. shareholder owns more than 50% of the foreign corporation’s stock, therefore controls the foreign corporation. They are related parties.

- If percentage is not more than 50%, continue.

- IRC §954(d)(3)(A) cannot not make the U.S. shareholder a related party to the foreign corporation.

- If the percentage is more than 50%, stop. You have your answer: your U.S. shareholder is a related party to the foreign corporation.

- From your previous analysis (where you computed the stock ownership that your U.S. shareholder has in the foreign corporation), you computed the U.S. shareholder’s total stock ownership percentage in the foreign corporation: direct, indirect, and constructive ownership as defined in IRC §958(a) and IRC §958(b).

- Check for IRC §954(d)(3)(B) related party status.

- Identify a common shareholder of the U.S. shareholder and the foreign corporation.

- If a common shareholder exists, continue.

- You will need to determine there whether the common shareholder owns more than 50% of both the U.S. shareholder and the foreign corporation.

- If no common shareholder exists, stop. You have your answer: the U.S. shareholder is not related to the foreign corporation.

- You are only examining IRC §954(d)(3)(B) because you previously determined that IRC §954(d)(3)(A) did not make the U.S. shareholder a related party to the foreign corporation.

- IRC §953(d)(3)(B) does not create related party status because there is no common shareholder who could possibly create related party status.

- Because neither IRC §954(d)(3)(A) nor IRC §954(d)(3)(B) create related party status, your U.S. shareholder cannot be related to the foreign corporation.

- Determine whether the common shareholder owns more than 50% of the U.S. shareholder, by vote or value.

- If yes (the common shareholder owns more than 50% of the U.S. shareholder), then continue.

- If no (the common shareholder does not own more than 50% of the U.S. shareholder) then stop. Conclusion: the U.S. shareholder is unrelated to the foreign corporation.

- You are only examining IRC §954(d)(3)(B) because you previously determined that IRC §954(d)(3)(A) did not make the U.S. shareholder a related party to the foreign corporation.

- Now you have proved that it impossible for IRC §954(d)(3)(B) make the U.S. shareholder be a related party to be satisfied since the common shareholder must own more than 50% of both the U.S. shareholder and the foreign corporation, and the common shareholder does not own more than 50% of the U.S. shareholder.

- Determine whether the common shareholder owns more than 50% of the foreign corporation, by vote or value.

- If yes (the common shareholder owns more than 50% of the foreign corporation’s stock, by vote or value), then stop. You have your answer: the U.S. shareholder is related to the foreign corporation.

- In step 2 you proved that the common shareholder owned more than 50% of the U.S. shareholder.

- In step 2 you proved that the common shareholder owned more than 50% of the foreign corporation.

- Therefore you have proven that the U.S. shareholder is related to the foreign corporation as provided in IRC §954(d)(3)(B) because a common shareholder controls both of them.

- If no (the common shareholder does not own more than 50% of the foreign corporation, then stop. You have your answer: the U.S. shareholder is not related to the foreign corporation.

- In step 2 you proved that the common shareholder owned more than 50% of the U.S. shareholder.

- In step 2 you proved that the common shareholder did NOT own more than 50% of the stock of the foreign corporation.

- Therefore, it is impossible for IRC §954(d)(3)(B) to be true because the common shareholder must own more than 50% of both the U.S. shareholder and the foreign corporation, and it does not.

- If yes (the common shareholder owns more than 50% of the foreign corporation’s stock, by vote or value), then stop. You have your answer: the U.S. shareholder is related to the foreign corporation.

Next time, we pull it all together

Tune in again in two weeks when we pull it all together in Installment 5: the Grand Unified Theory of Category 5.

- How you decide that you have a Category 5 problem.

- How you decide whether your Category 5 problem is a Category 5a, 5b, or 5c problem.

- The filing exceptions for Category 5 in Notice 2018-13 and Rev. Proc. 2019-40