- Article Category

- Trusts

- Published on

Is the Foreign Employees' Trust Exempt from U.S. Income Tax Under §501(a)?

Phil Hodgen

Attorney, Principal

Share

Summary

(This is the draft of Chapter 6 of my in-progress book on U.K. SIPPs).

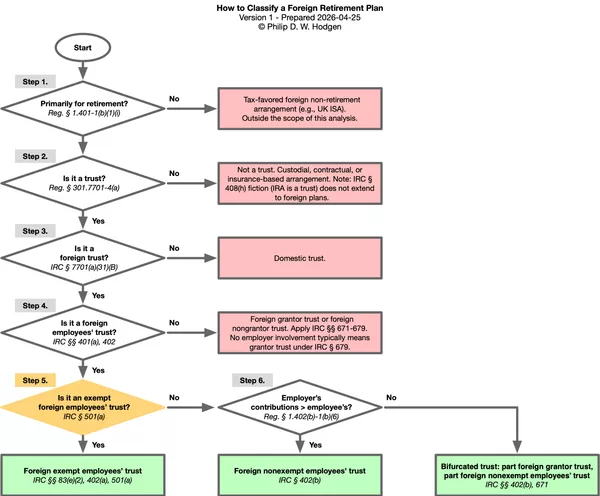

A U.K. SIPP is a foreign employees’ trust. It is NOT an exempt employees’ trust. By reaching this conclusion, we identify IRC § 402(b) as the Code section that determines how a U.S. participant in a U.K. SIPP is taxed.

Back Story

We have already determined that the SIPP holds its money in a trust - an employees’ trust, to be exact. The employee is, therefore, a beneficiary of a trust. How is that employee taxed?

We have already determined that the normal rules for taxation of distributions from foreign nongrantor trusts will not apply to employees’ trusts. Therefore, the rules of DNI and UNI and all that excitement will not apply. IRC §§ 641-669. And the rules for grantor trusts will not apply, either. That’s IRC §§ 671-679. (There is one exception to this rule, for bifurcated employees’ trusts, that will be discussed in Chapter 7. In some instances, an employees’ trust will be partly treated as a grantor trust).

So with the normal trust rules out of the picture, what are the rules for taxation of beneficiaries of employees’ trusts? They are found in IRC § 402:

- If the employees’ trust is an exempt employees’ trust, apply the rules of IRC § 402(a).

- If it is NOT an exempt employees’ trust, apply the rules of IRC § 402(b).

A UK SIPP is not–and can never be–an exempt employees’ trust. The reasons are explained below.

Therefore, we will determine the U.S. employee’s U.S. tax treatment by looking in IRC § 402(b). Subsequent chapters of this book will explain how, under IRC § 402(b), a U.S. participant in a U.K. SIPP will be treated for U.S. income tax purposes on employer contributions, plan earnings, and distributions.

What an exempt employees’ trust is

A trust that meets the requirements of IRC § 401(a) is a “qualified trust.” A qualified trust is exempt from taxation except for various exceptions (like unrelated business income) and exclusions (like those in IRC §§ 502, 503). IRC § 501(a).

You may see “qualified trust” and “exempt trust” used interchangeably, and that’s fine. For our purposes, I am going to use the term “exempt trust” to indicate that we are talking about a trust that satisfies all of the requirements of IRC § 401(a) and threads the needle of exemption under IRC § 501(a).

IRC § 401(a) defines a qualified trust:

An exempt trust is:

Why a UK SIPP Can Never Be a Qualified Trust

A UK SIPP can never be a qualified trust as defined in IRC § 401(a) for an existential reason: UK law requires a UK trust to be established for a SIPP, controlled by a UK trustee. A trust is a domestic trust if and only if two things are true:

- a court in the United States is able to exercise primary supervision of the trust’s administration (the court test), and

- all substantial administrative decisions are controlled by U.S. persons (the control test).

See Reg. §301.7701-7(a)(1), (2).

If either (or both) of these statements are false, then the trust is classified as a foreign trust. See Reg. §301.7701-7(a)(2).

By U.K. law, both of these requirements of U.S. tax law are impossible. A U.K. trustee is mandated, and any complaints about the administration of a SIPP must be resolved in U.K. courts.

But Wait! There’s an Exception!

There is an exception to the rule. A foreign trust can be an exempt trust in limited circumstances. IRC § 402(d) says:

This exception says that a foreign trust–like a SIPP–can be an exempt trust under IRC § 501(a) even if it is not a qualified trust under IRC § 401(a), in one limited circumstance. The SIPP must in all other ways be a qualified trust (i.e., it satisfies the 39 requirements) and if it does, it will be a qualified trust even though it is a foreign trust.

As discussed below, Parliament self-evidently did not design SIPPs to cater to the whims of Congress as written in IRC § 401(a). Therefore, a SIPP will not satisfy the IRC § 402(d) exception, and cannot be classified as an exempt trust under IRC § 501(a).

A SIPP Cannot Satisfy the 39 Specific Requirements of IRC § 401(a)

The SIPP’s classification as a foreign trust is enough to prevent it from “qualified trust” status under IRC § 401(a). But let’s be complete in determining the SIPP’s fate. In addition to being a domestic trust, a “qualified trust” must meet all of the 39 specified requirements listed in IRC § 401(a).

The 39 requirements, listed at IRC § 401(a)(1)-(39) constitute the thicket of rules that ensure that retirement plans cannot discriminate, limit contributions to the plans, and control when distributions occur–as well as other matters. All we need to do is ask ourselves a simple question: “Is it possible that U.K. SIPPs were designed to specifically and obsessively satisfy the statutory and regulatory requirements necessary to qualify the SIPP for U.S. tax-exempt status and keep that status up-to-date with every amendment of the Internal Revenue Code, every promulgated Treasury Regulation, and every burp of the Federal Administrative Beast?”

And to ask that question is to answer it. There is zero possibility that a SIPP will satisfy all 39 of the requirements of IRC § 401(a).

A SIPP is Definitely Not an Exempt Trust

A SIPP can never be a “qualified trust” under IRC § 401(a) because it is a “foreign trust” and because even without analysis we know that the SIPPs operational terms and conditions cannot meet the 39 enumerated requirements in IRC § 401(a). The exception to the rule that might allow a SIPP to be a “qualified trust” will not apply.

Because a SIPP is not a “qualified trust” it cannot be exempt from taxation under IRC § 501(a); in other words, it cannot be an “exempt trust.”

Implications for a U.S. Participant in the SIPP

The U.S. employee-participant in an exempt employees’ trust is subject to the tax rules specified in IRC § 402(a). If the employees’ trust is not exempt from tax under IRC § 501(a), then the U.S. employee-participant determines his or her income tax using the rules of IRC § 402(b).

Having identified the precise Code section that dictates the tax consequences to the employee-participant, in the following chapters we will explore how a U.S. employee-participant in a SIPP is taxed on employer contributions, plan earnings, and plan distributions.