- Article Categories

- US Real Estate Investments, US Tax Filings

- Published on

Filing Obligations for a Foreign Grantor Trust That Owns U.S. Rental Real Estate

Phil Hodgen

Attorney, Principal

Share

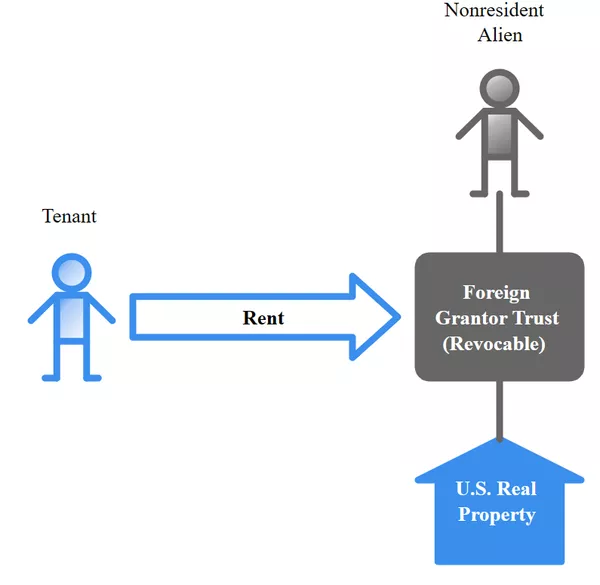

Nonresidents buy U.S. rental real estate. Sometimes they get their tax advice from their real estate agent and create a simple revocable trust to own the property.

Suboptimal tax planning, to be sure. But you, the accountant, are presented with a problem: what does this nonresident’s income tax return look like? What does your checklist look like? This week I got a sanity-check email from a return preparer on exactly this type of structure.

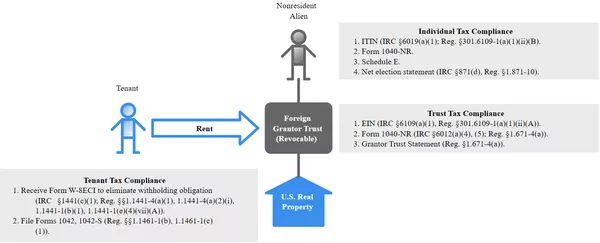

Here’s what the IRS expects to see:

That little graphic gives you the checklist you need. What follows is the explanation of why.

Why You See This Structure

The usual reason for using a revocable trust as the title-holding entity is to eliminate probate proceedings in the event of the nonresident’s death. California (where I live) is the poster child for why you would use a revocable trust: administering an estate through the Probate Court may be exceedingly slow, but at least it’s horribly expensive. The purpose of a system is what it does.

Sidenote: Why This Structure is Dumb (Retained Interest)

Not part of this episode, but just so you know why this structure is horrible and you shouldn’t use it: the power to revoke the trust means that the nonresident alien has a retained interest in the trust assets. IRC §2038.

That means if the nonresident alien–in a moment of poor judgment–decides to die, the U.S. real estate will be included in his/her gross estate and be subjected to estate tax. IRC §§2101, 2103, 2104(a). Bad news.

But as I said, people get their tax advice from the damndest places.

Meanwhile, it’s tax season and you have tax returns to file. You’ll talk to them about estate tax later.

Type of Taxpayer: Foreign Grantor Trust

Grantor Trust

A revocable trust is a grantor trust, and all of the income and expense items will ultimately be reported on the income tax return of the trust’s owner. Who is the owner?

- The nonresident alien is the trust’s grantor because (1) he/she created the trust and (2) also because he/she made a gratuitous transfer to it. Reg. §1.671-2(e)(1).

- The nonresident alien grantor is the trust’s owner of the trust because he/she is a grantor who made a gratuitous transfer to the trust (Reg. §1.671-2(e)(1)) and also holds the power to revest assets in his/her own name. IRC §676(a).

- Usually, foreign persons cannot be the owner of a trust. IRC §672(f)(1). But holding the power to arbitrarily revest assets in his/her own name allows the nonresident alien–despite being a foreign person–to be the “owner” of the trust. IRC §672(f)(2)(A)(ii).

Because the nonresident alien is the trust’s owner, all items of income and expense are directly included in his/her gross income. IRC §671. We call this type of trust a “grantor trust.”

Foreign Trust Trusts are classified as domestic if:

- they pass the court test (the correct court to settle a beef about the trust is in the United States) and

- they also pass the control test (all “substantial” decisions are controlled by U.S. persons). Reg. §301.7701-7(a)(1)(i), (ii).

If a trust is not domestic, it must be foreign. Reg §301.7701-7(a)(2).

The power to revoke a trust is pretty substantial, right? It’s the power of life or death over a trust. And a nonresident alien holds that power, right? Therefore, at least one substantial power is held by a non-U.S. person, and the trust is foreign.

Now What?

So we have a foreign grantor trust. It owns U.S. real estate that is collecting rent. Next, onward to income tax return filing obligations.

Foreign Grantor Trust: Income Tax Return

Apply for (and receive) an EIN. Prepare Form 1040-NR. Attach a grantor trust statement. File.

Tax Return Must Be Filed

Trusts (grantor or nongrantor) with gross revenue above $600, and trusts with nonresident alien beneficiaries, must file U.S. income tax returns. IRC §6102(a)(4), (5). This trust will probably toggle both.

Use Form 1040-NR

The IRS has authority to tell us what forms to use. IRC §6011(a). The IRS has told us to use Form 1040-NR. See the Instructions for Form 1041 (2025), page 6, and the Instructions for Form 1040-NR (2025), page 17. As far as I know, “use Form 1040-NR” is not in the Regulations.

Attach a Statement to Form 1040-NR

Because it’s a grantor trust, you do not report the items of income and expense on Form 1040-NR itself. Rather, you just attach a summary statement that gives all of the information that the trust owner needs to prepare and file an individual income tax return. Reg. §1.671-4(a).

There is no set format for what this statement should contain. The statement should give the owner of the trust sufficient information to prepare his/her income tax return. Sources of inspiration that show you what “complete” should look like:

- Schedule E. You’re going to be attaching this to the nonresident alien individual’s Form 1040-NR, so put every little piece of data you’d need for a complete individual Schedule E onto the grantor trust statement. (Do not attach Schedule E to the trust’s Form 1040-NR.)

- Foreign Grantor Trust Owner Statement. Form 3520-A, pages 3 - 4. This is for foreign grantor trusts with domestic owners, but it will work equally well for a foreign grantor trust with a foreign owner. Again, do not attach pieces of Form 3520-A to the trust’s Form 1040-NR.

- Notice 97-34. The canonical source of what a foreign grantor trust beneficiary statement should contain.

I emphasize: roll your own statement. Don’t attach Schedule E, and don’t adapt/attach the Form 3520-A foreign grantor trust owner statement. We all have first-hand horror stories about how mail is handled at the IRS Service Centers.

Practical advice: basically, a pretty version of the Schedule E workpapers will be sufficient.

At the top, state clearly: “Grantor Trust Information Statement Pursuant to Treas. Reg. §1.671-4(a) — All items of income, deduction, and credit shown below are reportable by the grantor, [Name], ITIN [XX-XXXXXXX], on the grantor’s Form 1040-NR.”

EIN Required

All tax returns must have a taxpayer identification number on them. IRC §6109(a)(1). The identifying number for a trust is its employer identification number. Reg. §301.6109-1(a)(1)(ii)(A).

Filing Deadlines, Extension

Since the foreign trust files Form 1040-NR, the filing deadlines for nonresident aliens will apply. This is an inference unsupported by Code or Regulations. The Instructions for Form 1040-NR (2025) say:

The trust itself will almost certainly not have an office in the United States. The investment asset (rental real estate) is not an office. Therefore, June 15 is your deadline.

The extension of time for an individual is for 6 months from the filing deadline. Reg. §1.6081-4(a). Although the regulation does not say so, we can infer that it applies to trusts as well as individuals, because we are told to use Form 1040-NR. Six months from June 15 is December 15. File your Form 4868 using the usual process.

Since a lot of this is inference from sloppy rules from the IRS, the safe practice is to get Form 4868 on file before April 15.

The Nonresident Alien Individual: Tax Return

The grantor trust rules attribute 100% of the trust’s income to the nonresident alien. IRC §671.

Income Tax Return

If the nonresident is engaged in U.S. trade or business at any time in the year, a tax return is required even if there is no effectively connected income from the business. Reg. §1.6012-1(b)(1). Since your nonresident individual has almost certainly made the net election under IRC §871(d) to be deemed engaged in trade or business, file an income tax return no matter what. Failure to do so might torpedo the ability to take deductions against income. IRC §874(a).

If the nonresident is not engaged in trade or business in the United States for rental activity, then the rental income is FDAP. A tax return is required if the tax liability is not satisfied in full by withholding at source. The withholding rate is 30%. IRC §1441(a). I have never seen a situation where a tenant has withheld 30% of rental income and remitted the withheld amount to the IRS with Form 1042 and Form 1042-S.

Therefore, as long as there is rental activity or rental income, an income tax return will be required for the nonresident alien individual.

ITIN

A taxpayer filing an income tax return needs a taxpayer identification number. IRC §6109(a). You will need to apply for and receive an ITIN for the nonresident alien. IRC §6109(d), Reg. §301.6109-1(d)(3).

Schedule E

Income and expense items are reported on Schedule E, derived from the grantor trust statement attached to the revocable trust’s Form 1040-NR.

Tenant Withholding/Reporting Issues

The tenant is a withholding agent. IRC §7701(a)(16), Reg. §1.1441-7(a)(1). A lessee of property is explicitly a withholding agent. Reg. §1.1441-7(a)(2). The tenant must withhold 30% of the rent paid because it is “FDAP” income by default. Reg. §§1.1441-2(a), 1.1441-7(a)(1).

The tenant does not need to withhold tax on the rental payments if the income is effectively connected with a U.S. trade or business. Reg. §1.1441-4(a)(1). This is why nonresident landlords should always make the net election to make the rental income into effectively connected income. The landlord must deliver Form W-8ECI to the tenant for the tenant’s reliance purposes. Reg. §1.1441-4(a)(2).

The tenant has a reporting requirement, even if the withholding requirement is eliminated by the landlord delivering Form W-8ECI to the tenant. Form 1042 is required for amounts paid to foreign persons, even if no tax was withheld. Reg. §1.1461-1(b). Form 1042-S, too. Reg. §1.1461-1(c)(2)(i)(A) explicitly calls out ECI payments as being reportable.

In reality, nobody does any of this. Imagine your average Toyota mechanic who rents an apartment from you. Is he going to withhold 30% and remit it to the IRS and file Form 1042 and Form 1042-S? Does he even know that the landlord is a nonresident alien?

In practice, the nonresident alien landlord should interpose a domestic property manager to receive rent from the tenant. Then the withholding and reporting obligations imposed on the tenant go away. The Form 1042 and Form 1042-S reporting obligation falls on the property manager, and can be handled privately and efficiently.