- Article Category

- Trusts

- Published on

Is It a Bifurcated Foreign Employees' Trust?

Phil Hodgen

Attorney, Principal

Share

Summary

A SIPP is an employees’ trust, but like all things tax, there is an exception to that statement. In some circumstances an employees’ trust will be split into two parts:

- Part will be treated as a grantor trust owned by the employee; and

- The rest will be treated as an employees’ trust.

The split occurs only if the employee’s cumulative contributions to the SIPP exceed the employer’s cumulative contributions. And like all things tax, it’s easy to state a general rule, but in application of the rule, details are lacking.

Back Story

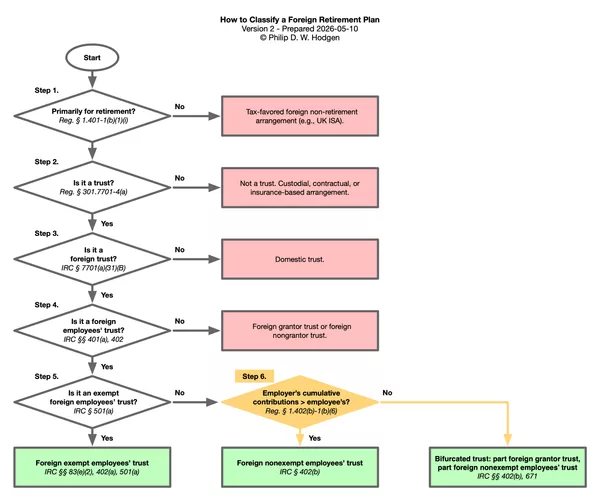

Here is the flowchart that shows the analytical process to follow in deciding how the U.S. will tax an employee who participates in a foreign retirement plan. We are at Step 6.

The SIPP is a retirement plan (created primarily for retirement purposes) and not some other tax-favored account, like an ISA. We have decided that it is a foreign employees’ trust. And we have decided that a SIPP is not an exempt employees’ trust.

There is one more step we need to analyze. We have a nonexempt employees’ trust, which means that IRC §402(b) dictates the income tax treatment of the employee/beneficiary of that SIPP.

That step is Step 6 in the flow chart, and depending on your analysis, you will decide that one of two results is true:

- 100% of the SIPP is a foreign nonexempt employees’ trust, with IRC §402(b) governing the employee’s taxation on contributions, plan earnings, and distributions (the “Yes” answer to the Step 6 question); or

- Some of the SIPP is a foreign nonexempt employees’ trust, and part of the SIPP is a foreign grantor trust with the employee as the owner of that portion of the trust (the “No” answer to the Step 6 question).

The Bifurcation Rule

The General Rule: IRC §402(b)(3)

The general rule is simple: an employees’ trust is never treated as a grantor trust with the employee treated as the owner.

IRC §402(b)(3) says:

Reg. §1.402(b)-1(b)(6) echoes the general rule from IRC §402(b)(3) but sneaks in a weasel word (emphasis added to highlight it):

“Incidental” opens the door to an exception that obliterates the general rule.

Exception to the General Rule: Reg. §1.402(b)-1(b)(6)

Reg. §1.402(b)-1(b)(6) then introduces the exception: if employee contributions are not incidental, then the employee is the owner of a portion of the employees’ trust. The Regulation says (emphasis added):

“Incidental” is defined as “employee’s cumulative contributions exceed the employer’s cumulative contributions.” The Regulation says:

Synthesizing the Code and the Regulation, we end up with a straightforward rule:

- Employer’s cumulative contributions exceed the employee’s cumulative contributions: 100% of the SIPP will be a foreign nonexempt employees’ trust.

- Employee’s cumulative contributions exceed the employer’s cumulative contributions: a portion of the SIPP will be treated as a foreign nonexempt employees’ trust, and the remainder will be treated as a grantor trust with the employee classified as the owner.

Employer Contributions vs Employee Contributions

There are four ways that contributions can be made to a SIPP. This section describes whether the U.S. tax rules will treat them as employer contributions or employee contributions for purposes of Reg. §1.402(b)-1(b)(6).

Relief at Source: Employee Contribution

A SIPP member making a contribution using the relief at source method uses his or her own after-tax cash. Through an inscrutable system that only a bureaucrat could love, HMRC then tops up the SIPP with a 20% basic-rate addition, treated as a refund of basic-rate income tax that the member is deemed to have paid on the gross contribution. The top-up is paid directly into the SIPP. Higher- and additional-rate taxpayers receive the further 20% or 25% of relief separately, as a refund (or reduced tax bill) on Self Assessment — paid to the member personally, not to the SIPP.

For Reg. § 1.402(b)-1(b)(6), this is an employee contribution. Both the cash from the member’s bank account and the HMRC top-up are attributable to the member: the cash is hers directly, and the top-up is her own income tax relief routed through the SIPP. The employer is nowhere in the transaction.

Direct Employer Contribution: Employer Contribution

Think of the typical 100%-owned limited company whose shareholder is the sole employee. The limited company (or whoever employs the member) makes a payment from corporate funds straight to the SIPP.

For Reg. § 1.402(b)-1(b)(6), this is an employer contribution. The money came from corporate funds and never passed through the employee’s hands — it was never her wages, never her cash, never an amount she had a contractual right to demand.

Salary Sacrifice: Employer Contribution

The next way that money finds its way into a SIPP is by salary sacrifice. An amount that the employee would otherwise have received as salary is paid directly into the SIPP instead. This requires a legally binding contractual variation of the employment contract.

This is conceptually the same as the U.S. “cash or deferred election” concept. The analogous U.S. situation is an employee’s instructions to an employer about how much salary should be deposited in a 401(k) plan instead of paid to the employee as income. In such a case, IRC §401(k) classifies the employee’s elective contribution to the 401(k) plan as employer contributions. See, e.g., Reg. §1.401(k)-6, which defines “elective contributions” as follows:

The reason §401(k) treats an elective deferral as an employer contribution is that the deferral election eliminates the employee’s right to receive the deferred amount as cash; with no right to the cash, there is no actual or constructive receipt by the employee. UK salary sacrifice works the same way: the contract variation extinguishes the employee’s right to the income before she earns it. Reg. § 1.402(b)-1(b)(6) applies to nonexempt employees’ trusts, not exempt employees’ trusts (like a 401(k) plan). Nevertheless, the same concepts for classifying a contribution as an employer contribution or employee contribution should apply. Exempt or nonexempt status matters for determining the taxation of the plan participants, not for determining the source of contributions to an employees’ trust.

Therefore, the salary sacrifice contribution to a SIPP will be an employer contribution.

Third Party Contributions: Employee Contribution

Sometimes the money going into a SIPP doesn’t come from the worker or her boss. It comes from somebody else — a parent, a spouse, a grandparent, a friend, anyone.

Example: Sarah has a SIPP. Her dad wants to help her save for retirement. Dad deposits £80 to Sarah’s SIPP.

What happens next is exactly the same thing that would have happened if Sarah had deposited the funds herself. This is a variation on the relief at source system described above.

- The £80 goes into Sarah’s SIPP.

- HMRC adds £20 on top via Relief at Source, so Sarah’s SIPP ends up with £100.

- If Sarah is a higher-rate UK taxpayer, Sarah (not Dad) claims the extra higher-rate relief on her tax return and gets a direct additional tax refund.

UK law pretends Sarah made the contribution herself. The legal phrase from HMRC’s manual is: “any contribution that is not an employer contribution will be regarded as if it had been made by the scheme member.”

For Reg. § 1.402(b)-1(b)(6), this is an employee contribution. The money did not come from Sarah’s employer, so it cannot be an employer contribution. The cleanest way to think about it under US tax principles: pretend that Dad made a gift to Sarah (not taxable to her under IRC § 102), and then pretend that Sarah contributed Dad’s gift to her SIPP. The result is the same as a regular relief at source contribution: it is an employee contribution.

You might hate the deemed gift idea. You might say the substance-over-form argument is that Dad is a third-party contributor and the contribution should be analyzed on its own terms: neither an employer contribution nor an employee contribution, but a third category that Reg. § 1.402(b)-1(b)(6) does not expressly contemplate. After all, parents make gifts to trusts for the benefit of their children all the time, and we don’t play “let’s pretend” to re-attribute the trust contribution to the child-beneficiary.

This is an analytically honest footgun. If Dad’s contribution falls outside the IRC § 402(b) framework, the portion of the SIPP funded by Dad is a foreign nongrantor trust as to Sarah:

- The SIPP is a foreign trust.

- We’ve decided that IRC §402(b) rules will not apply to Dad’s contribution, because he is not an employer or an employee. Employees’ trust status is out.

- Dad is not a US person, so the grantor trust rules do not make him the owner of the SIPP.

- Sarah did not transfer the property, so she is not a grantor either, and therefore cannot be the owner of the trust under the grantor trust rules.

- The last man standing for determining the U.S. tax treatment of distributions from the SIPP? It’s a foreign nongrantor trust.

When Sarah eventually takes a distribution, the throwback tax of IRC § 665-668 applies to accumulated income, with the punitive interest charge and the loss of long-term capital gains rates. This is the worst of all possible worlds.

I recommend Option 1, the deemed gift theory, for at least two reasons.

- First, it tracks the UK statutory characterization, which expressly deems third-party contributions to be member contributions; aligning the US characterization with the UK characterization avoids the cognitive dissonance of having two tax authorities call the same transaction by two different names.

- Second, it keeps the analysis inside the IRC § 402(b) nonexempt employees’ trust framework, which is at least mapped territory. Jumping off the train tracks of IRC §402(b) and taking the dirt road of foreign nongrantor trusts is apt to take you somewhere you don’t want to go, and there is little-to-no mapping of the intersection of retirement plans and foreign nongrantor trust rules, so you will be making things up as you go along.

The deemed gift theory is the better answer for the SIPP holder, and absent contrary IRS guidance it is a defensible position. This is not legal advice, etc.

Conclusion

Step 6 asks one question: do the employee’s cumulative contributions to the SIPP exceed the employer’s cumulative contributions? If yes, the SIPP is bifurcated: part is a grantor trust owned by the employee, and the rest is a foreign nonexempt employees’ trust governed by IRC § 402(b). If no, the SIPP is 100% a foreign nonexempt employees’ trust and the entire SIPP runs through the IRC § 402(b) framework.

The four contribution methods sort cleanly under this rule.

- Relief at Source contributions and third-party contributions land on the employee-contribution side.

- Direct employer contributions and salary sacrifice land on the employer-contribution side.

For the typical US-citizen limited company director-shareholder who funds her SIPP aggressively through corporate channels, employee contributions will almost always be incidental, the bifurcation rule never triggers, and the entire SIPP is IRC § 402(b) territory.

The bifurcation rule actually does work for SIPPs funded outside the employment relationship: the self-employed sole trader, the PAYE employee whose SIPP sits alongside a workplace pension, the non-working spouse, the SIPP funded by a parent or grandparent. In those cases the employee can be the owner of all or most of the SIPP under grantor trust principles.

There is an unhappy asymmetry here: the population most aware of the IRC § 402(b) problem is the population for which bifurcation almost never triggers, and the population for which bifurcation actually does work is the population least likely to know they have a US tax issue at all.