- Article Category

- IRS Form 5471

- Published on

Subpart F Income in a Multi-Level Structure, Episode 3

Phil Hodgen

Attorney, Principal

Share

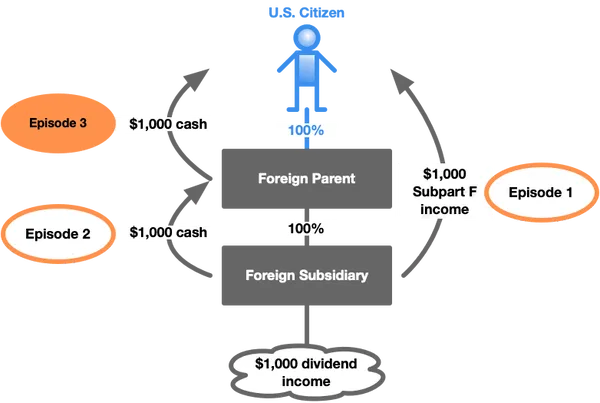

This is Episode 3 of a series where we track $1,000 of subpart F income by a lower-tier CFC subsidiary, with cash distributions all the way up the stack to the U.S. shareholder--and see what happens.

Catching up on this series

In our previous two episodes, we traced $1,000 of dividend income (aka subpart F income) earned by a foreign subsidiary.

- Episode 1 showed the tax effect on the U.S. shareholder. Bottom line: $1,000 of gross income on the U.S. shareholder's income tax return.

- Episode 2 of this series showed what happens when the foreign subsidiary pays a $1,000 dividend to its foreign parent corporation. Bottom line: no impact on the U.S. shareholder.

- Now, in Episode 3, I show you what happens when the foreign parent corporation pays a $1,000 dividend to the U.S. shareholder.

Step 1. We have a double-taxation problem

Our U.S. shareholder will have $1,000 of cash and $2,000 of taxable income. That's a problem. Fortunately, the Code fixes the problem.

IRC §301(c) says that if a shareholder takes a distribution from a corporation as dividend income to the extent of the paying corporation, then the distribution is a return of capital (reducing basis), then capital gain.

This is a distribution to U.S. shareholder from earnings and profits of Parent (the earnings and profits came from the dividend received from Subsidiary). Therefore, this is dividend income for the U.S. shareholder. IRC §301(c)(1).

Step 2. Prevent double-taxation with E & P hot potato

A distribution of previously-taxed earnings and profits will not be included in U.S. shareholder's gross income. IRC §959(a). Therefore, if the dividend from Parent to U.S. shareholder is from previously-taxed earnings and profits, we can exclude it from U.S. shareholder's gross income.

Foreign Parent's earnings and profits are classified as previously-taxed earnings and profits. The earnings and profits were previously taxed at the Subsidiary level. The character of the earnings and profits, when distributed up the holding structure, remains the same. The earnings and profits are a hot potato – "previously-taxed earnings and profits" – all the way up until the U.S. shareholder receives it.

Reg. §1.959-3(b), in relevant part, gives the answer:

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi

Therefore, Foreign Parent has earnings and profits that are previously taxed -- specifically allocated to the IRC §959(c)(2) bucket, if you're a bucket nerd like I am -- and for the year in which the inclusion occurred.

Bottom line: Parent has $1,000 of previously-taxed earnings and profits, and $1,000 of cash.

$1,000 of cash.

Step 3. Distribution from PTEP is not included in U.S. shareholder's gross income

When Parent distributes $1,000 of cash to U.S. shareholder, it is a dividend because it is a distribution of earnings and profits. But it is a distribution from previously-taxed earnings and profits.

Because it is a distribution from previously-taxed earnings and profits, the $1,000 dividend income is excluded from U.S. shareholder's gross income. IRC §959(a)(1).

We have solved the double-taxation problem:

- The subpart F income from Subsidiary is included in U.S. shareholder's gross income.

- The dividend income from Parent is not included in U.S. shareholder's gross income.

But we have created another double-taxation problem in its place. :-)

Step 4. Distribution reduces Shareholder's basis in Parent stock

The dividend from Parent to U.S. shareholder is not included in gross income for the U.S. shareholder. As a result, it is treated as a return of capital, which reduces U.S. shareholder's basis in Parent stock. IRC §§301(c)(2), 961(b).

Reducing basis in Parent stock means higher capital gain when Parent stock is sold later. That means the $1,000 of dividends received by Subsidiary created $1,000 of subpart F income for U.S. shareholder and a future $1,000 of capital gain when the Parent stock is sold.

This is not pleasant: out of the double-taxation frying pan (subpart F income plus dividend income) and into the double-taxation fire (subpart F income plus capital gain).

Step 5. Solve the double-taxation problem by an offsetting basis adjustment

- 961(a) gives the U.S. shareholder a transitive basis adjustment upward for the subpart F income included below.

- 961(b) gives the U.S. shareholder a basis adjustment downward for the cash distribution received.

- Now there is no net change in the U.S. shareholder's basis, therefore we have not created a change in the eventual capital gain on sale of the Parent stock.

Conclusion

Over the three episodes in this series, we traced $1,000 of dividend income received by a CFC subsidiary.

Episode 1

- Subsidiary earned $1,000 of dividend income (we pretended this was a Nestlé dividend).

- The dividend income is foreign personal holding company income, which is foreign base company income, which is subpart F income.

- The U.S. shareholder included the $1,000 of subpart F income in gross income. IRC §951(a)(1)(A).

- The U.S. shareholder increased his basis in Parent stock by $1,000. IRC §961(a).

Episode 2

- Subsidiary paid a $1,000 dividend to Parent.

- The dividend came from Subsidiary's from previously-taxed earnings and profits.

- Therefore, the dividend is excluded from gross income of Parent. IRC §959(b).

- This means that the dividend did not create new subpart F income for Parent.

- Parent has earnings and profits because of the dividend received, but the earnings and profits carry the same characteristics as they had with Subsidiary: previously-taxed earnings and profits.

Episode 3

- Parent distributed $1,000 cash to U.S. shareholder. This is a dividend to the shareholder.

- The distribution is from previously-taxed earnings and profits of Parent.

- Therefore, U.S. shareholder does not include the dividend in gross income. IRC §959(a).

- U.S. shareholder reduces his basis in Parent stock by the amount of the distribution received. IRC §§301(c)(2), 961(b)(1). This offsets the earlier and equal upward adjustment in Parent stock basis triggered by inclusion of subpart F income of Subsidiary included in U.S. shareholder's gross income.

End result

- $1,000 of Nestlé dividends received by Subsidiary results in $1,000 of subpart F income to U.S. shareholder.

- $1,000 cash decants up the holding structure to U.S. shareholder without affecting U.S. shareholder's taxable income.