- Article Category

- IRS Form 5471

Updated Posted

American Minimultinationals: An Introduction

Phil Hodgen

Attorney, Principal

Share

What's an American Minimultinational?

What do I mean by American minimultinational?Multinational

A multinational business operates in multiple countries, exposed to multiple tax-hungry governments. Apple. General Motors. Exxon.A minimultinational is a multinational business, but smaller.- Do you have 100 people in a cubicle farm working on your international tax stuff? You're a multinational.

- Is that thought ludicrous bordering on insane? You're a minimultinational.

American

An American minimultinational is one that is owned by a U.S. citizen or resident.Merely by having a U.S. citizen or green card holder as an owner, a business that operates 100% outside the United States is a multinational business. It is exposed to the tax system of the country where it operates (because it's based and operating in that country), and it is exposed to the U.S. tax system because of the citizenship/resident status of its owner.- The company might be based in the United States and do business abroad.

- Or it might be entirely based abroad — with no customers or business activities in the United States. These are the companies that interest me most.

In summary

- American because the company is based in the USA and does business abroad, or because a 100% foreign business is owned by an American citizen or resident.

- Minimultinational because the company is bigger than a lemonade stand and smaller than General Motors.

Who?

The series is for American entrepreneurs living abroad, running normal businesses. Specifically, you have a business that looks approximately like this:- You’re an American citizen or green card holder. You own a business.

- It’s a normal, everyday business. Could be a tech operation, could be a janitorial service.

- It’s profitable. Let’s arbitrarily use a threshold of $1 million/year profit.1

- You probably don’t have a CFO, or if you do, your CFO doesn’t have the time or training to devote to U.S. tax planning.

Complexity

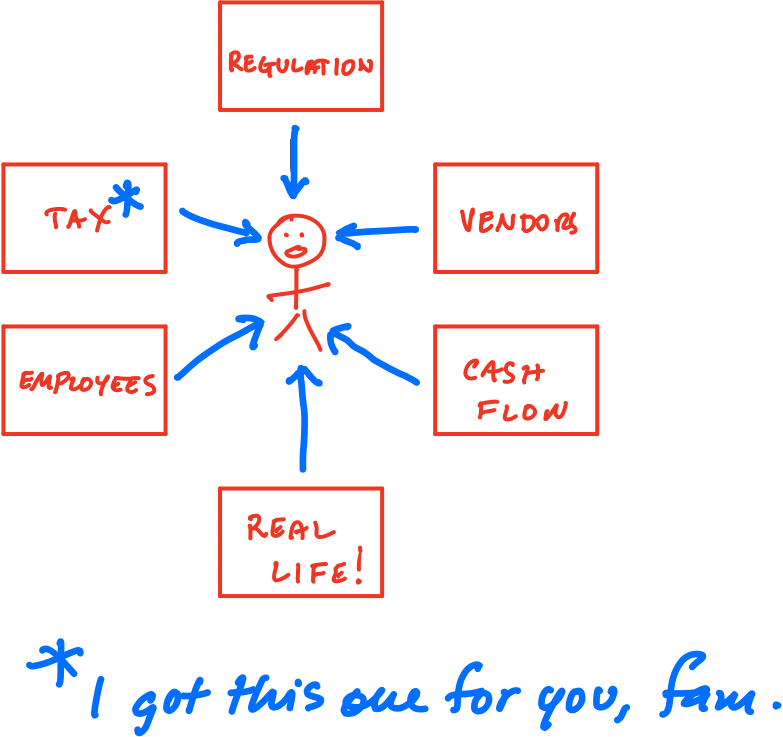

More to the point, you are squeezed by complexity from all sides. I know that life because I live that life. :-)This series is intended to give you, the American entrepreneur, just enough information to make good decisions on how to remove (tax) complexity from your life.

I know that life because I live that life. :-)This series is intended to give you, the American entrepreneur, just enough information to make good decisions on how to remove (tax) complexity from your life.Why a problem exists

The United States asks its citizens and residents to pay U.S. tax on their worldwide income.2The request extends to the businesses that American taxpayers own. Thanks to a dramatic change in U.S. tax law, it is likely that most of an American minimultinational's net profit will be taxable in the United States every year.In a nutshell:- Your personal income is taxable in the United States, no matter where you live and where you earn it; and

- Your company's net profit is (probably) taxable in the United States, even if you have no business operations in the United States at all.

The upcoming episodes

Here's where we're going with the series. Remember that I reserve the right to change things as I go. And I will definitely take input from you, dear reader, about places to go and dead ends to avoid.01. Overview of the series

- Tax concepts overview. What are the features of U.S. tax law that make running an American minimultinational so brutal?

- Structures overview. Why choosing a business structure correctly makes such a big difference in outcomes.

- Introduce the default structure we will look at: a U.S. citizen lives abroad, owns 100% of a foreign corporation that is engaged in business in the country of residence.

- Give a preview of the coming attractions.

02. Why business profit is (mostly) taxable

- The types of business profit you (as an owner) will be taxed on, even if your business doesn't distribute a dime of cash to you.

- With a minimum of jargon, explain how the tax rules these types of business profit work.4

03. Cash distributions

- Your foreign corporation had business profits that you paid U.S. tax on. Then it paid you a dividend. Do you pay tax again? Maybe! Let's look at the impact of choosing the right business structure.

04. Good corporations, bad corporations

- The U.S. tax system sees good foreign corporations and bad foreign corporations: Controlled Foreign Corporations and Passive Foreign Investment Companies.5

- I attempt to explain it all ELI5-style. You will decide whether I succeed.

05. An overview of structure choices

- An overview of the different structures you can choose for your American minimultinational.

- What are the criteria you use to judge whether one structure is better than another? Less tax, sure. But what else?

06. Just use a U.S. corporation

- A discussion of how a U.S. citizen living/working abroad uses a U.S. corporation to run a minimultinational.

07. Direct ownership of a foreign corporation

- The classic default situation for a U.S. citizen entrepreneur living abroad. You form a corporation in your home country because that's how people do business.

- What are the U.S. tax consequences?

08. Direct ownership plus Section 962

- The classic default situation for a U.S. citizen entrepreneur living abroad. You form a corporation in your home country because that's how people do business.

- But you don't like the U.S. tax consequences. Here's a special election that might/might not help.

09. Sole proprietorship or disregarded entity

- What if you get rid of the corporation? It's a dreadful source of tax complexity and potential penalties. Just do business as you--a sole proprietor.

- Or if you need a business entity, make a special tax election to make your foreign company invisible (mostly) for U.S. tax purposes.

10. Parent/subsidiary

- This is probably the new default "best idea" for American minimultinationals: a U.S. holding corporation that owns your foreign corporation. How does it work? What are its benefits? What are its drawbacks?

11. Dual-resident corporation

- You know about people who hold two passports, right? Dual citizens. Well, you can do the same thing with corporations. A company can simultaneously be a domestic limited company for U.K. tax purposes and a domestic corporation for U.S. tax purposes. Cool, no? We will look at this strategy and see if it saves tax, reduces paperwork, and mixes fine cocktails for happy hour.

12. Conclusion and "Into Action"

- Wherein we wrap up loose ends and explore concrete "next action" steps that the American entrepreneur can take.

- Plus I will try to hardwire a cliff-hanger into the plot to get you to return for Season 2.

- Don’t worry if your business is larger or smaller. The ideas we will discuss scale up and down to apply to you, too. ↩

- The man from the IRS shows up at your door, wearing a cheap suit. He carelessly brushes open his jacket as he talks to you, revealing a concealed sidearm. ↩

- For those of you who love tax jargon, this is Subpart F income and GILTI. ↩

- Hat tip to Funkadelic's classic "Good Thoughts, Bad Thoughts". This is the extended version of the song so you can hear all of the glorious guitar work. If you have never heard of Eddie Hazel and you think you have heard every guitar genius ever, think again. ↩