- Article Category

- IRS Form 5471

- Published on

Demystify Category 5a/5b/5c, Installment 3 - What Kind of Shareholder Are You?

Phil Hodgen

Attorney, Principal

Share

The Series

Completed installments

. If you understand how the IRS tried to fix what Congress broke, the whole exercise of figuring out which (sub)category applies will be a bit easier.

. Is your foreign corporation a “foreign-controlled CFC” or a “U.S.-controlled CFC” and why does this matter? (Hint: U.S.-controlled CFCs go straight to Category 5a.)

This installment

Installment 3: What Kind of Shareholder Are You? Is your United States shareholder a “section 958(a) U.S. shareholder” or a “constructive U.S. shareholder”?

Future installments

Installment 4: Related or Unrelated? Is your United States shareholder “related” or “unrelated” to the foreign-controlled controlled CFC?

Installment 5: Checking the Right Box. We pull it all together. You will know whether your United States shareholder is a Category 5a, 5b, or 5c filer, or maybe you hit the jackpot—and the Category 5 filing requirement is waived entirely.

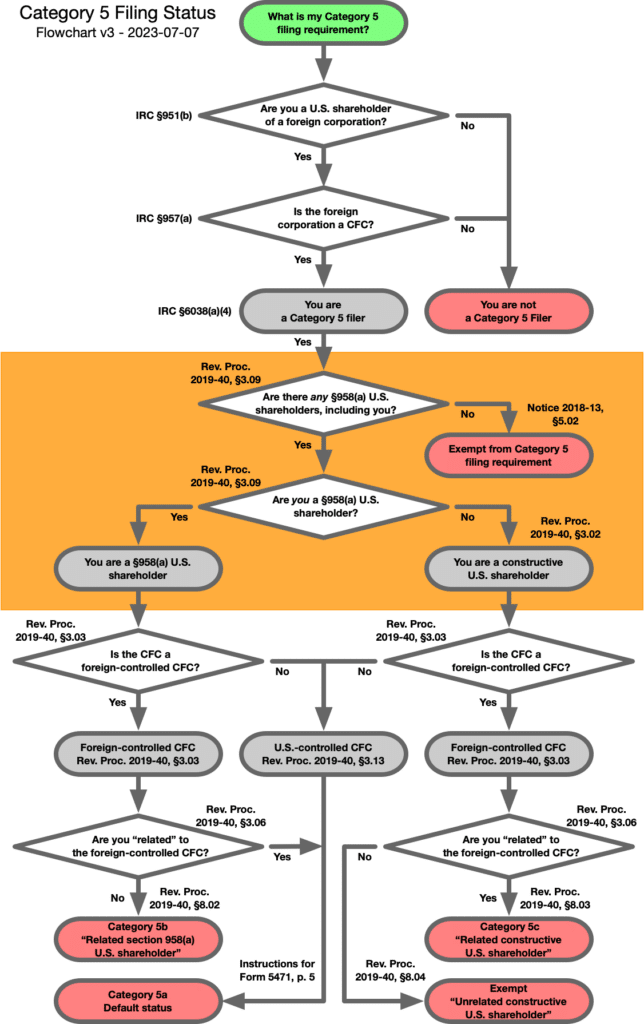

The Flowchart

The flowchart shows you the analytical steps to take to determine your Category 5 filing obligation. (This flowchart has been slightly updated. The steps are the same but I have tweaked the wording here and there to make things a bit clearer, and updated/added references to published authority).

This week I cover the steps highlighted in orange.

What kind of shareholder are you?

There are three types of stock ownership for controlled foreign corporations:

Direct ownership [IRC §958(a)(1)(A)]

Indirect ownership through a foreign entity [IRC §958(a)(1)(B)]

Constructive ownership [IRC §958(b)].

Don’t worry. You have already done the work. You already computed the stock ownership when determining your status as a United States shareholder, and the foreign corporation’s classification as a controlled foreign corporation.

Why does it matter?

Remember what the objective is here: the IRS is giving you a break in your Form 5471 compliance burden in Rev. Proc. 2019-40.

They are using two ways of determining how much clout you have — in order to force the foreign corporation to give you data needed to complete your Form 5471 obligations:

How your own the foreign corporation stock that made you a U.S. shareholder. (Discussed today).

Whether you are related or unrelated to the foreign corporation. (Discussed next time).

If you, a constructive U.S. shareholder, go knock on the foreign corporation CFO’s door and demand financial data for your Form 5471. Uncle Sam’s attribution rules are nothing to a CFO of a corporation in India. The CFO may know the shareholder whose stock is attributed to you. But you? Who are you? You are a stranger and will likely get a brusque GTFO, at best.

On the other hand, if you are a direct shareholder (or an indirect shareholder through a holding company, perhaps), the CFO will know who you are. You have some sort of economic investment in the corporation. With luck and a winsome smile, you might even cajole the data you need from that harried CFO, sufficient to keep the IRS happy on your Form 5471.

Question 1. Are there any section 958(a) U.S. shareholders?

Start with the top diamond shape in the orange-shaded area. Your answer to this question will identify a possible Category 5 filing exception.

Exception: no section 958(a) U.S. shareholders

If the foreign corporation has no section 958(a) U.S. shareholders at all, then you do not have a Category 5 filing requirement. The Instructions for Form 5471 (rev. 01-2023) describes the exception, at page 6:

No section 958(a) U.S. shareholder. A Category 5 filer does not have to file Form 5471 if no U.S. shareholder (including the Category 5 filer) owns, within the meaning of section 958(a), stock in the CFC on the last day in the year of the foreign corporation in which it was a CFC and the CFC is a foreign-controlled CFC. See section 5.02 of Notice 2018-13, 2018-6 IRB 341 for additional information.

What’s a section 958(a) U.S. shareholder?

Rev. Proc. 2019-40, Section 3.09 defines section 958 U.S. shareholder:

The term "section 958(a) U.S. shareholder" means, with respect to a foreign corporation, a U.S. shareholder with respect to the foreign corporation that owns (within the meaning of section 958(a)) stock of the foreign corporation.

It can be any amount of stock owned within the meaning of IRC §958(a).

You could own one puny share of stock directly (as defined in IRC §958(a)) and enough shares of stock constructively (as defined in IRC §958(b)) to bring you to or above the magic 10% stock ownership level to be a U.S. shareholder.

That would make you a section 958(a) U.S. shareholder as that term is defined in Rev. Proc. 2019-40.

Why does this filing exception exist?

Because it applies to a situation where there will never be tax revenue, so the paperwork would be pointless for you to prepare and the IRS to process.

Only U.S. shareholders who own CFC stock as defined in IRC §958(a) will include Subpart F income or Global Intangible Low-Taxed Income in their gross income.

If all of the U.S. shareholders (you included) own their stock constructively as defined in IRC §958(b), the government will never collect a nickel of tax from any of the U.S. shareholders (including you) of the CFC.

Technically, IRC §6038(a)(4) requires all U.S. shareholders of a CFC to be Category 5 filers--even if stock ownership is purely constructive. This exception overrules IRC §6038(a)(4) in situations where there will never be tax revenue generated from the CFC.

Your checklist

Here’s what to do:

Create a complete picture of all U.S. shareholders, how much stock they own, and how they own it (directly, indirectly, or constructively).

If you have access to stock ownership data, use it.

If you do not have access to stock ownership data and you can use the safe harbor at Rev. Proc. 2019-40, Section 4 to take a position that the foreign corporation is not a CFC, you have solved the problem. You are a U.S. shareholder of a foreign corporation, but you are not a U.S. shareholder of a controlled foreign corporation. The safe harbor lets you do that. Therefore you do not have a Category 5 filing requirement.

If you do not have access to stock ownership data and the safe harbor does not apply, I don’t know what to tell you. Sorry. I think you have to assume this filing exception does not apply.

Determine if any of them (including you) own stock directly or indirectly in the foreign corporation, as defined in IRC §958(a).

If definitely yes (i.e., at least one U.S. shareholder owns stock in the foreign corporation directly or indirectly as defined in IRC §958(a)), proceed to Question 2. This filing exception does not apply to you.

If definitely no (i.e., there are no U.S. shareholders who own stock in the foreign corporation directly or indirectly as defined in IRC §958(a)), apply the filing exception to eliminate your Category 5 filing requirements.

If you can’t tell for sure, I think you have to assume that someone is a section 958(a) U.S. shareholder, kiss this exception goodbye, and resign yourself to some kind of Category 5 filing requirement. Proceed to the Question 2.

Question 2. Are you a section 958(a) U.S. shareholder?

Remember why we are here:

You previously determined that you are a U.S. shareholder of a foreign corporation.

You previously determined that the foreign corporation is a controlled foreign corporation.

There is at least one section 958(a) U.S. shareholder of the controlled foreign corporation.

Are you are a section 958(a) U.S. shareholder?

You already know the answer. You know whether you own stock directly or indirectly (within the meaning of IRC §958(a)) in the foreign corporation. All you need to do is follow the checklist to see what your answer to this question means.

Your checklist

Are you a U.S. shareholder of a foreign corporation?

Are you a section 958(a) U.S. shareholder, as defined in Rev. Proc. 2019-40, Section 3.09, of the foreign corporation?

If the answer is “yes” then you are a section 958(a) U.S. shareholder.

If the answer is “no” then you are not a section 958(a) U.S. shareholder. And if you are not a section 958(a) U.S. shareholder, then you are a constructive U.S. shareholder.

Conclusion

That’s all you need to do in this step. The three outputs possible from your work are:

No Category 5 filing requirement because there are no section 958(a) U.S. shareholders at all (including you). A filing exception applies.

You are a section 958(a) U.S. shareholder. You have some type of Category 5 filing requirement to be determined. Or maybe there is a filing exception that applies.

You are a constructive U.S. shareholder. Again, you have a Category 5 filing requirement of some kind, or perhaps you get lucky with a filing exception.