- Article Category

- Cross Border Business

- Published on

Why the Disregarded Entity Election is not Necessarily a Good Idea

Phil Hodgen

Attorney, Principal

Share

The Punchline

If you want to skip the appetizers and go straight to dessert:

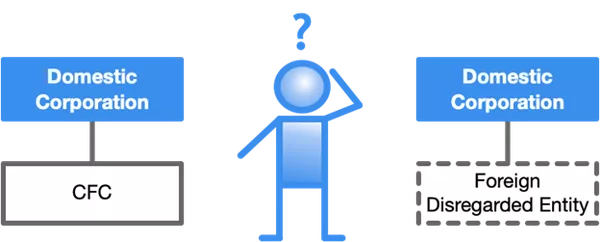

Consider a U.S. corporation doing business abroad.

- If it conducts its business through a foreign disregarded entity, the income is taxed on Form 1120 at 21%.

- If it conducts its business through a CFC (and assuming it’s the right kind of income and the wind is blowing in the right direction), the income will be taxed at 10.5%.

Why the effective tax rates are different:

- The CFC’s global intangible low-taxed income inclusion on Form 1120 will qualify the domestic corporation for 50% of the income inclusion. Section 250(a)(1)(B).

- The foreign disregarded entity’s income will not create any foreign-derived intangible income qualifying the domestic corporation for the 37.5% deduction. Section 250(a)(1)(A).

Why there is no foreign-derived intangible income:

- Because the foreign disregarded entity’s income is “foreign branch income” and the way the math is set up (see Form 8993, line 2f) means that the income base to compute foreign-derived intangible income is zero.

- And 37.5% of zero is zero.

Why I wrote this newsletter

Because this week I learned I was wrong.

What happened

Faced with a choice of “would I rather pay for Form 5471 or would I rather pay for Form 8858?” a domestic corporation made a check-the-box election for a wholly-owned foreign subsidiary.

Everything went smoothly until the return preparer (a friend of mine) looked at Form 8993 and wondered why the software was not giving her a Section 250 deduction for the foreign profits from the disregarded entity.

She emailed me. And several hours of enlightenment (for me) later, here we are.

Zealot

I have been a zealot for choosing passthrough entities. Form 8832 yay.

This little problem-solving exercise showed me that passthroughs are not necessarily all good. Here is a situation where reflexively choosing a passthrough structure created in a higher effective tax rate on foreign profits.

To quote noted international tax scholar H. L. Mencken, “For every complex problem there is an answer that is clear, simple, and wrong.”

My reflexive belief that passthrough entities are the answer? Simple and wrong.

New, improved (and humbled) POV

Lesson learned: you can’t say that a disregarded entity election is good or bad until you run the numbers. Use Excel, use your tax software to model different scenarios.

But run the numbers.

CFC or disregarded entity? Which to choose?

Here’s a taxpayer trying to choose between two structures: foreign operations conducted through a CFC or a foreign disregarded entity.

CFC gets a Section 250 deduction

Assume the foreign business operations are such that they generate income that falls into the global intangible low-taxed income category if earned by a CFC. That income is then included in the U.S. shareholder’s gross income because of IRC Section 951A(a).

The U.S. shareholder gets a deduction, too. Section 250(a)(1)(B) gives a domestic corporation a tax deduction – 50% of the amount of global intangible low-taxed income inclusion.

This creates an effective tax rate of 10.5% ($100 of income minus a $50 tax deduction = $50 of taxable income x 21% = $10.50).

Disregarded entity: no Section 250 deduction

The same foreign business activities conducted by a foreign disregarded entity will generate an income inclusion on the domestic corporation’s Form 1120. “Taxable on worldwide income” and all that. Reg. Section 301.7701-2(a) says:

A business entity with only one owner is classified as a corporation or is disregarded; if the entity is disregarded, its activities are treated in the same manner as a sole proprietorship, branch, or division of the owner.

But the domestic corporation will not be entitled to will not generate a Section 250(a)(1)(A) deduction of 37.5% of foreign-derived intangible income.

IRC Section 250(a)(1) In general. In the case of a domestic corporation for any taxable year, there shall be allowed as a deduction an amount equal to the sum of (A) 37.5 percent of the foreign-derived intangible income of such domestic corporation for such taxable year[.]

As a result, the income generated by the foreign disregarded entity will be taxed at the full 21% corporate tax rate.

Why no Section 250 deduction?

The Section 250 deduction isn’t banned, explicitly, when you're doing business through a foreign disregarded entity. There's nothing obvious that says so. Instead, the equations are tilted to yield a $0 deduction.

Simple financial statement

Assume the following simple P & L for the foreign disregarded entity:

- gross revenue = $100,000

- deductions = $0

It provides services to persons living outside the United States.

The P & L for the domestic corporation is even simpler. It has no other activity except the business activity of the foreign disregarded entity.

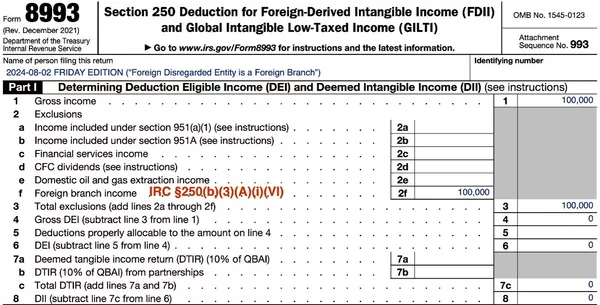

Form 8993 shows you what happens

If you look at Form 8993, lines 1 through 6, you can see an interesting thing happening.

- The domestic corporation's gross income is on line 1.

- The foreign disregarded entity’s gross income is deducted from the domestic corporation’s gross income (see line 2f) to compute a number labeled DEI (no, not that DEI—this is Deduction Eligible Income).

The $100,000 gross income for the domestic corporation is on line 1. That income is foreign branch income, so it is included on line 2f.

Drop down to line 4, and Gross DEI is $0. So is DEI on line 6.

Without getting into the nerdy details of how foreign-derived intangible income is calculated, let’s just say there is a “multiply by a fraction” mathematics operation in the calculation. DEI (“deduction eligible income”) is part of the fraction. And if DEI is zero, the fraction reduces to zero. And if the fraction is zero, anything multiplied by the fraction is zero. The fraction is used to compute Foreign-Derived Intangible Income, so that type of income must be zero. And the Section 250(a)(1)(A) deduction is therefore 37.5% of zero. Also zero.

And that’s how we get to the result of a $0 value Section 250 deduction for domestic corporations deriving income from foreign branches.

I have an overly pedantic write-up of how this works, and I will publish it separately for the Scholars amongst you. I wrote it to learn how it works. It's a combination of 8th grade algebra, college-level symbolic logic, and caffeine.

Why is this “foreign branch income?”

How do you know that income generated by a foreign disregarded entity doing business abroad is “foreign branch income”? In other words, why am I so sure that the foreign disregarded entity's income finds a home on Form 8993, line 2f?

“Foreign branch income” means business profits from a Qualified Business Unit in a foreign country. IRC Section 904(d)(2)(J)(i).

So, the question now becomes “is a foreign disregarded entity a Qualified Business Unit?” If yes, and if the Qualified Business Unit is in a foreign country, then its business profits will be "foreign branch income." And (oh look, what a coincidence!) "foreign branch income" goes on Form 8993, line 2f.

A Qualified Business Unit needs two things to exist:

- Activities that constitute a trade or business, and

- A separate set of books for those activities.

See Regs. §1.989(a)-1(b)(2)(ii).

The foreign disregarded entity will, without question, qualify as a Qualified Business Unit. It has business activities, and it must have a separate set of books from its owner to satisfy the tax reporting obligations in the foreign country.

And the foreign disregarded entity’s income will be “foreign branch income” because the disregarded entity is a Qualified Business Unit generating profits from activities in a foreign country.

Therefore, the foreign disregarded entity’s gross revenue will be excluded from gross revenue on Form 8993, line 2f as “foreign branch income” in computing the domestic corporation’s Gross DEI. IRC Section §250(b)(3)(A)(i)(VI).

The real question: “What business structure should I choose?”

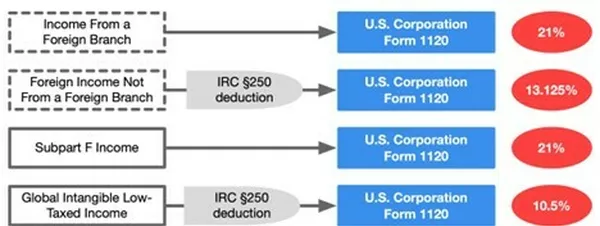

I have just demonstrated that a foreign disregarded entity will pass its income through to its domestic corporation owner; tax will be imposed at 21% with no Section 250 deduction.

When looking at alternatives, let’s just say that the U.S. tax laws are a bit of a shambles—just looking at income tax rates.

Depending on the structure choice (CFC or foreign disregarded entity) and the income type, a dollar of profit from foreign business operations might be taxed at 10.5%, 13.125%, or 21%.

There are, of course, many other structure possibilities.

And it may be possible for you to push and shove reality so that Global Intangible Low-Taxed Income looks like Subpart F income instead. Or vice versa. And don't forget the high-tax exception.

All I'm saying here is that one of the factors in the structure selection game is the income tax rate. There are other factors, and you have a number of buttons you can push. Personally, I'm a big fan of pushing the foreign tax credit button.