- Article Category

- US Real Estate Investments

- Published on

How to Give Notice of a FIRPTA Nonrecognition Transaction to the IRS

Phil Hodgen

Attorney, Principal

Share

Today I give you a little bit of practical FIRPTA goodness when you have a nonrecognition transfer of U.S. real property by a nonresident. My example is property held in a domestic LLC that makes a check-the-box election to be classified as a corporation. There’s a paperwork requirement, and frankly it is a bit difficult to figure out what and how to do it.

Check-the-box elections and IRC Section 897

A nonresident might form a domestic LLC to own U.S. real estate. And for one reason or another, it might be useful to make a check-the-box election to classify that LLC as a corporation rather than accept its natural tax classification as a disregarded entity.

That check-the-box election is a potential footgun.

The check-the-box election is treated as a contribution of assets and liabilities of the LLC to a corporation in exchange for stock. Reg. §301.7701-3(g)(1)(iv). And this, of course, smells like a classic IRC §351 nonrecognition transaction: a capital contribution to a corporation in return for stock.

IRC Section 897(e)(1) says nonrecognition provisions cannot be used for dispositions of U.S. real property interests by nonresident individuals or foreign corporations. And IRC §351 is a nonrecognition provision for purposes of IRC §897. Temp. Reg. §1.897-6T(a)(2).

Therefore, this check-the-box election is a “disposition” of a U.S. real property interest by the nonresident sole member of the LLC, and gain is recognized by the nonresident. IRC §897(a)(1).

But of course there is an exception

Of course there are exceptions. And one of them applies neatly to this situation. IRC §351 will be allowed to provide nonrecognition treatment if three things are true.

Some other time I will tell you why a check-the-box election satisfies the first two requirements (the USRPI for USRPI transfer, and the "it's taxable immediately after the transfer" thing). I’m only going to talk about the paperwork—the “filing requirements of paragraph (d)(1)(iii) of § 1.897-5T.”

The paperwork is a tad convoluted

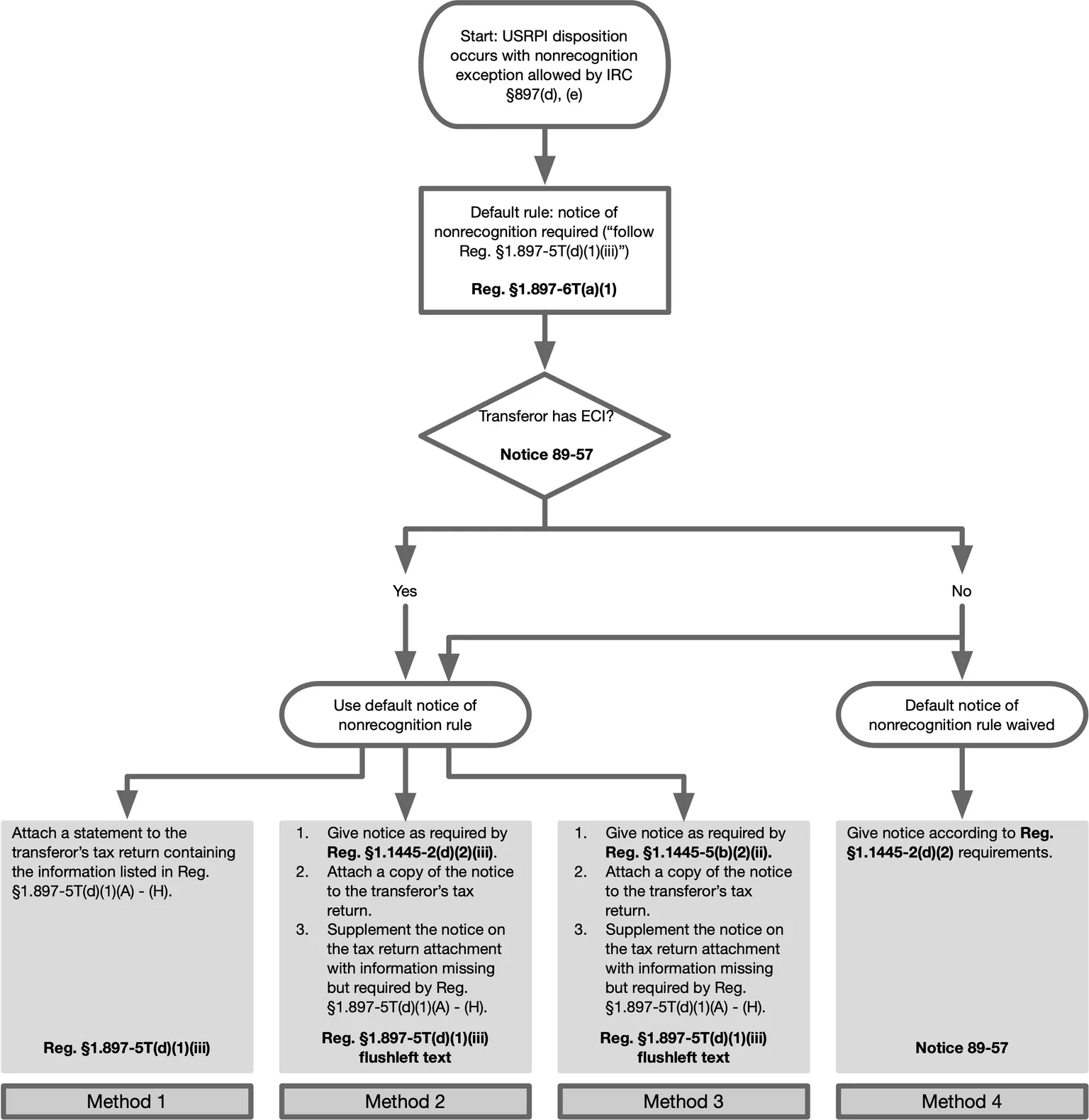

The paperwork requirement is harder to understand than you think. You need to start with Temp. Reg. §1.897-5T(d)(1)(iii), then apply the cumulative effect of Notice 89-57, Notice 89-85, Notice 99-43, and Notice 2006-46. Fortunately, only Notice 89-57 applies here.

And remember. The Notices are not Gospel. You can always rely on the Regulations and ignore the Notices if you want to. (Hint: see my conclusion--I think you should do just that).

Here is a handy decision tree to show what kind of paperwork is required to make a nonrecognition provision work with a disposition of U.S. real estate by a nonresident or foreign corporation.

Methods 1, 2, and 3—the default notice of nonrecognition methods

Reg. §1.897-5T(d)(1)(iii) gives you three different ways to give notice of a nonrecognition transaction. Remember: if you don’t give notice, you don’t get nonrecognition for your transaction!

Method 1

Attach a statement to the transferor’s income tax return for the year of the transaction. Answer the questions in Reg. §1.897-5T(d)(1)(A) – (H) in the statement.

This is simple: do your transaction (file Form 8832 to make the check-the-box election), bolt a statement onto the transferor’s income tax return. Done.

Method 2

This is found in the flushleft language at the bottom of Reg. §1.897-5T(d)(1)(iii).

If you have filed a notice of nonrecognition under Reg. §1.1445-2(d)(2)(iii) (more about that below), attach it as a statement to the transferor’s income tax return. The notice won’t answer all of the questions in Reg. §1.897-5T(d)(1)(iii)(A) – (H), so answer those questions in a statement attached to the income tax return, too.

The Reg. §1.1445-2(d)(2)(iii) notice of nonrecognition is something that the transferor gives the transferee to prevent the FIRPTA withholding requirement. That’s pretty easy in a check-the-box election situation: the LLC member gives the notice to the LLC.

The trick is that the transferee, within 20 days of the transfer, is supposed to send a copy of the notification received to the IRS. Reg. §1.1445-2(d)(2)(i). That means the LLC (the transferee) sends the IRS a copy of the notice it received from the sole member (the transferor).

Technically, the only requirement in Temp. Reg. §1.897-5T(d)(1)(iii) is to “. . . [provide] . . . a notice described in § 1.1445-2(d)(2)(iii) . . . .” Technically, that does not include the transferee's letter to the IRS.

When I have used this method I figured it was worth the extra effort to have the transferee send the notice to the IRS, certified mail, return receipt requested.

This method is a bit fussy, a bit ambiguous, and doesn’t really save you a lot of work. Even if you do everything I describe above, you still have to attach the notice of nonrecognition to the transferor’s tax return, and add anything missing from the list at Reg. §1.897-5T(d)(1)(iii)(A) – (H).

I am kinda meh about this, TBH. But I've done it.

Method 3

This is another method found in the flushleft language at the bottom of Temp. Reg. §1.897-5T(d)(1)(iii). If you have filed a notice under Reg. §1.1445-5(b)(2)(ii) (more about that below), you attach it to the income tax return as a statement, and answer the unanswered questions in Temp. Reg. §1.897-5T(d)(1)(iii)(A) – (H).

Method 3 is for distributions of U.S. real property interests by corporations, partnerships, trusts or estates. That’s not relevant to our particular fact pattern here (a check-the-box election by a disregarded entity).

Again, this is a bit fussy with lots of moving parts. I’m underwhelmed. The transferor is filing an income tax return anyway--why not just do the full statement required by Temp. Reg. §1.897-5T(d)(1)(iii)(A) – (H)?

Method 4

This one is legitimately less work.

You can skip the whole “attach a statement to the tax return” requirement entirely if the transferor satisfies the requirements of Notice 89-57:

The constraint that will catch you is that "does not have any other income that is effectively connected . . ." requirement. If the property in question is rental real estate, by definition there is effectively connected income.

However, if you meet all three conditions, then all you need to do is the Reg. §1.1445-2(d)(2) notification process.

The Reg. §1.1445-2(d)(2) notification of nonrecognition works like this:

- The transferor gives a notice of nonrecognition to the transferee. In my sample transaction, the sole member gives notice to the LLC that is making the check-the-box election. The information required for the notice of nonrecognition is detailed in Reg. §1.1445-2(d)(2)(iii). Reg. §1.1445-2(d)(2)(i)(A).

- Then, the transferee sends a copy of the notice of nonrecognition received, along with a cover letter to the IRS within 20 days of the transfer. Reg. §1.1445-2(d)(2)(i)(B). There are specific requirements for the cover letter.

This is probably easier than attaching a statement to the transferor’s income tax return, with answers to all of the items in Reg. §1.897-5T(d)(1)(iii)(A) – (H). My main fear is that the IRS denies ever receiving the letter. Sure, I have certified mail, return receipt requested proof of delivery. But even with that it is sometimes a pain to get the Service to admit that the letter actually arrived. (Let me show you my scars).

Conclusion

If you satisfy the requirements for Notice 89-57 (especially the “no effectively-connected income”, consider using Method 4. In my experience it is useful in limited circumstances (e.g., personal residences with no rental income).

However, I am heavily biased to attaching a statement to the income tax return and using the default method. Frankly, it’s not that much work to whip up the statement required by Reg. §1.897-5T(d)(1)(iii). You don’t have to worry about the 20-day deadline for sending a letter off to the IRS, and you don't have to worry about delivery.

Use Method 1. Do the statement.