- Article Category

- US Real Estate Investments

- Published on

Homes in Foreign Corporations: The Pit Boss Risk

Phil Hodgen

Attorney, Principal

Share

People prefer the cheap, expedient, and familiar – even when this means visible, latent risks. (I am a people, too).

This article is about one of those risks.

The big lesson of survivorship bias is that you should optimize for being a survivor.

I want you, the nonresident investor in U.S. real estate, to see, at least, a latent tax risk. Everything is fine now and has been for decades, because the Emperor is currently attending to other tasks. But there are tells . . . .

Nonresidents, their U.S. homes, and corporate structures

Nonresidents buy U.S. homes for personal use – by themselves, by family members. The homes are frequently owned by holding companies: non-U.S. corporations, or U.S. subsidiaries of non-U.S. parent corporations.

They do this because these structures are cheap, easy to understand, and leave them in full control of their investment.

First-order problem solved, second-order problem created

A corporate holding structure solves a first-order tax risk (estate tax exposure) but creates many second-order income tax problems.

One of the lesser second-order problems is imputed income: you (or a family member) lived in the house without paying rent, and the U.S. tax system sees an opportunity to impose income tax.

A taxpayer’s personal use of corporate assets has long been a happy hunting ground for the IRS. Vacation homes, airplanes, boats. Personal use of these corporation-owned assets has created constructive income for the individual and tax complexities for the corporate owner.

Theoretical or real?

Nota bene: this is mostly theoretical. I have watched 40 years of IRS activity and have not yet seen first-hand a nonresident investor with a home in a corporation face the tax risk I will describe here.

Conversations with other tax lawyers, an article in a professional journal here and there, a very few Tax Court cases . . . . well, the professional consensus is that there is something going on here, but no one is sure exactly what – so why worry?

But

But one of these days (YouTube) this attack may become a (cough) compliance initiative project (cough) at the IRS.

A couple of Tax Court cases are your tells: the government’s early efforts at organizing a litigation strategy. The IRS had some modest success.

Is obscurity (“Little ol’ me! How will the IRS ever find me!”) and an (at the moment) understaffed opponent still honing its strategy enough comfort for you? Maybe. You be the judge.

My thesis: (1) People – including tax professionals – underprice this second-order risk (meaning the cost of lawyers to fight the IRS, the cost of taxes, penalties and interest). (2) People are terrible at understanding probability, especially long-tail risks. Therefore, we take on more risk than necessary.

Most of the time it works out just fine, and (3) a good outcome is taken as proof that we are very smart.

No. We are wrong on this, too.

(I am a people, too!)

The first-order tax problem: estate tax

When a U.S. nonresident-noncitizen of the United States invests in U.S. real estate (or any U.S. asset, for that matter), the big obvious problem is the estate tax.

The estate tax is imposed on the value of assets owned by a person who dies. Insider tax pro jargon for the assets: “taxable estate”. Traditional legal jargon for a person who dies: a “decedent.”

The “taxable estate” is the value of everything the decedent owns (the “gross estate”) minus various deductions and exemptions.

The “gross estate” of a nonresident-noncitizen of the United States only includes assets located in the United States. (“Located” has a technical, non-intuitive meaning). U.S. real estate is self-evidently located in the United States. Owning it directly means the estate tax is imposed if the nonresident-noncitizen dies.

The solution to this risk is “If you are a nonresident-noncitizen, don’t own anything located in the United States.”

And a classically easy way to do this is to have the nonresident-noncitizen own all of the stock of a non-U.S. corporation.

- A corporation is considered to be “located” in its country of organization.

- Therefore, the asset owned by a decedent (stock of a non-U.S. corporation) is considered to be located in the corporation’s country of organization – even if the assets owned by the corporation itself are U.S. assets.

This leads to partly-informed tax planning decisions: Bahamas corporation that owns U.S. real estate will eliminate the U.S. estate tax risk. Yay! We're done.

When the nonresident-noncitizen shareholder of that Bahamas corporation dies, his gross estate includes the stock of that Bahamas corporation, not the U.S. real estate owned by the Bahamas corporation. You don’t look through a corporation and pretend that the shareholder owns the corporation’s assets.

That is why people like to use non-U.S. corporations to own U.S. real estate. They prevent the obvious estate tax risk.

The three corporate structure variants

I see three variants of this strategy. All three have the same estate tax benefit, but behave differently for operational and income tax purposes. In all cases, I show direct stock ownership of the non-U.S. corporation by a nonresident-noncitizen (of the United States) person, but the stock could be owned by a trust.

Direct ownership by a non-U.S. corporation

The first is direct ownership of U.S. real estate by a non-U.S. corporation. This seems to be common in legacy structures. (Translation: broken investment holding structures that I am asked to fix).

These structures are simple but can inject practical friction into ownership and sale of the real estate. Real estate is an inherently local industry, and local knowledge may not extend to knowing how to deal with the sale of real estate owned by a foreign corporation.

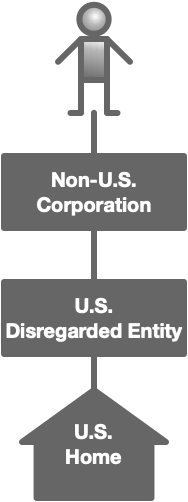

Two-tier, with LLC

The second variant is a two-tiered structure using an LLC that is classified as a disregarded entity for U.S. tax purposes.

This gives the advantage of a local company as the registered owner of the real estate–valuable for day-to-day ownership and operations, and a pathway to a simpler sale later. The income tax results of such a structure will be identical to direct ownership by a non-U.S. corporation.

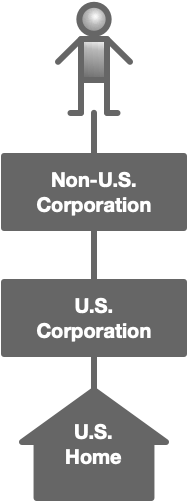

Two-tier, with corporation

The third is a two-tiered structure using a U.S. corporation to act as registered owner of the real estate. All of the stock of the U.S. corporation is owned by the non-U.S. corporation.

Income tax results now differ significantly from the other two holding structures, quite often in a good way. But let’s talk about that some other day.

The second-order effect: imputed income

Every action creates a reaction. Solving the estate tax risk problem introduces new U.S. income tax problems.

An artificial legal entity (the corporation) – by definition, engaged in business activities for profit – allows its assets to be used for free by its shareholders, officers, or family members of either.

If a corporation is engaged in business/investment (why else does a corporation exist, but to be engaged in economic activity for profit?) use of its assets must be profit-motivated in some way. What happens when someone uses the corporation’s assets without payment, for personal benefit?

Hilarity ensues

Canadian tax law is explicit in imposing a “let’s pretend” dividend on the shareholder. The U.S. system is muddling toward that solution, I think. At the moment we are in the “muddling” phase where the IRS is trying to hack together arguments without an explicit provision in the (U.S.) Internal Revenue Code along the lines of Subsection 15(1) of the (Canadian) Income Tax Act.

I well remember the impact on Canadians who owned winter hideaway homes in Palm Springs, Palm Desert, La Quinta etc. when Subsection 15(1) was enacted. Hilarity ensued for those who held title to their houses in corporate structures, let’s just say. Suddenly, they faced current personal Canadian income tax because of the way they owned their homes in the California desert.

I don’t want you to get caught in a “hilarity ensued” situation when the U.S. tax system catches up with its Canadian counterparts.

The legal theories

There are two theories the government uses to attempt to impose income tax in situations like this.

The constructive distribution method

A shareholder who uses a corporation-owned house rent-free could be treated as having made a deemed payment of rent to the corporation, followed by a deemed distribution (dividend, if it is paid from earnings and profits) to the shareholder.

In a sense, this is like the below-market loan fictions of IRC §7872. An interest-free loan to a child, for instance, is treated as if the borrower-child paid deemed interest to the lender-parent. The “let’s pretend” interest payment to the lender-parent is “funded” by a “let’s pretend” gift of an equivalent amount of money from the lender-parent.

There is a 2012 Tax Court case where the deemed distribution method worked: G.D. Parker v. Commissioner. A nonresident owned 80% of a Panama corporation, which owned a Florida subsidiary, which in turn owned another Florida subsidiary. Rent-free use of U.S. residential property, the Tax Court decided, triggered a deemed distribution from subsidiary to parent corporation.

The G.D. Parker opinion is a bit muddled and incomplete. No matter. Don’t second-guess a Tax Court judge and figure out whether the decision is right, wrong, or something in the middle.

All you need to know is that the IRS thought of the constructive distribution attack and won a partial victory against a nonresident who had a vacation home in Florida (among other things) in a corporate structure.

The IRC §482 method

The other way the IRS can attempt to tax rent-free personal use of corporate-owned real estate is by using IRC §482.

Section 482 – the transfer pricing statute – is the source of the IRS’s “I reject your reality and substitute my own” powers. It gives the government broad powers to reconstruct transactions between parties. It can create income where none previously existed.

Again, you do not need to become an expert in transfer pricing and the interpretation of the Code and Regulations. All you need to know is that the risk exists, and the government has tried to use it at least once.

Sparks Farm, Inc. v. Commissioner, T.C. Memo. 1988-492 is the case. A woman put her farm into a corporation, but continued to live rent-free in the farmhouse. The government attempted to argue IRC §482 created phantom income for the corporation. The Tax Court rejected the argument.

Incidentally, in Sparks Farm the Tax Court judge told the IRS “You lose on your IRC §482 argument, but if you had tried the constructive distribution argument it probably would have worked.” Take that as a fair warning.

Lawyer opinions do not affect reality

If you read the tax pro literature you will find smart people people arguing about the Sparks Farm opinion and the G. D. Parker case and whether the judges’ got it right or wrong, and why.

Again, all of that intellectual flexing is misplaced. You argue like when you’re in Court, behind the eight-ball already. Before that, you set up your life so you never have the problem in the first place. It is sufficient to see the potential problem and route around it.

The IRS goes on crusades (aka "probabilities")

A lawyer’s interpretation of the merits of the IRS’s constructive dividend argument or a transfer pricing-based argument is pointless. Just think of how the IRS has pushed its point of view on:

- Conservation easements;

- Family limited partnership estate planning techniques; and

- Valuation discounts.

I could probably think of more. The IRS decided Something Was Wrong and went after lots and lots of taxpayers to establish the precedent it wanted. (And if that fails, it can ask Congress to rewrite the Internal Revenue Code.

You are playing blackjack by the rules (picking a tax strategy) in a big casino (the United States of America) and winning (not paying "your fair share" of tax). The pit boss (the IRS) can kick you out of the casino, and the casino can change the rules of the game if you start winning too much.

The analogy I'm using tells you what I think about probabilities. Will the IRS audit you? If they audit you, will they win?

These are not the right questions to ask when your opponent writes the rules of the game.

The right question is: "Am I willing to accept a ruinous outcome if I lose?"

Pricing the risk

A friend of mine (now deceased) who had a triple-digit number of Tax Court trials under his belt told me one day that it took at least $150,000 of legal fees to get to the point of saying “Ready, Your Honor” on Day 1 of a trial. That’s a 20-years ago budget.

It’s easy for a tax lawyer to tell you to adopt an ambiguous position that he feels intellectually strongly about. You’re the one who will pay the legal fees to defend his conception of reality, and the taxes, penalties, and interest if he is wrong.

Again, calculating a number with precision is the wrong approach. The right approach is to avoid ruinous outcomes, up front.

People misunderstand survivorship bias. The point of survivorship bias is that you should optimize for survival.

What to do

So what do you do with all of this? Here's my philosophy. It applies to all tax questions – not just the semi-theoretical, incipient risk that I believe is coming (eventually).

- Don't think in probabilities ("What's the probability that I will get audited?") because we humans aren't terribly good at it. Think about avoiding ruin. h/t Nassim Taleb.

- Ask your tax advisor to tell you what "worst case" looks like. What could possibly go wrong and what will taxes, penalties, and interest look like? What about professional fees to fight the government? Can you live with that outcome?

- Resist your instinct to choose the easier, softer way. (I.e., cheap/simple corporate structures). Run upstairs. h/t Paul Graham. (I.e., choose the heavier-duty tax strategies instead).

Make Future You proud of the tough choices that Today You made.