- Article Category

- US Tax Filings

Updated Posted

When Do You File Form 5472 for a Domestic Single-Member LLC?

Phil Hodgen

Attorney, Principal

Share

This topic is from real life and will help you this tax season when confronted with a holding structure that looks like the one discussed here. When exactly do you file Form 5472 for a disregarded entity?

The subtle treachery of the Internal Revenue Code

Form 5472 is sometimes required for foreign-owned domestic disregarded entities. This is not easy to remember, because the Code's logic is a variation on Abraham Lincoln’s famous riddle:

How many legs does a dog have if you call his tail a leg? Four. Saying that a tail is a leg doesn't make it a leg.

Congress nevertheless sometimes calls a disregarded entity a corporation and requires Form 5472.

Real-life example

A local CPA friend asked me a question about a tax return on his desk. Rather than keep the conversation private, I figured I would publish the whole thing here. I hope it solves a problem for you, too.

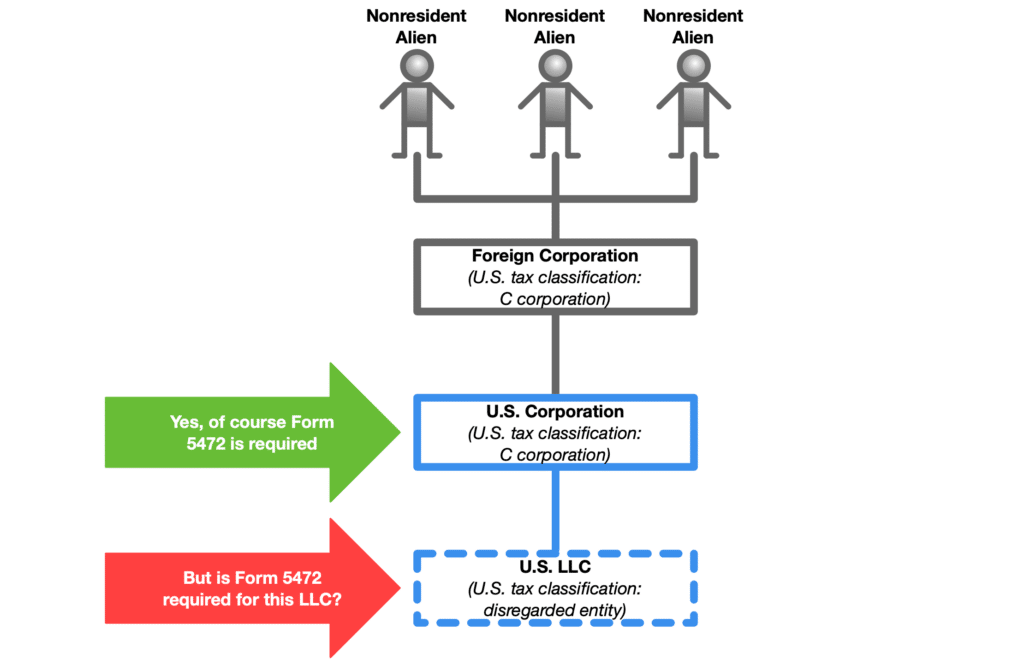

Here's the holding structure we discussed, suitably stylized, idealized, anonymized and simplified to protect the innocent.

Yes, it is a classic foreign parent corporation/domestic subsidiary structure, with a domestic LLC (classified as a disregarded entity) wholly owned by the domestic subsidiary.

Without question, Form 5472 will be required for the domestic subsidiary (assuming of course that there are “reportable transactions” with a “related party”).

But what about the LLC?

Does the LLC in this example file Form 5472?

What say you? Do you prepare and file Form 5472 for the domestic limited liability company or not?

True to Betteridge’s Law, the answer is no. My CPA friend need not prepare and file Form 5472 for a domestic LLC wholly owned by a domestic subsidiary of a foreign corporation.

Let's talk about why.

Why?

For people who just want the logic and the bullet points, here’s the answer:

- Form 5472 is filed by “reporting corporations” only.

- A “reporting corporation” is, of course, a corporation.

- Sometimes, an entity is classified as a disregarded entity and a corporation.

- Only some disregarded entities are classified as corporations for Form 5472 purposes.

- They must be the right kind of entity.

- They must have the right kind of foreign ownership.

- An LLC owned by a domestic corporation has the wrong kind of foreign ownership.

- It does not have a direct sole foreign owner.

- It does not have an indirect sole foreign owner because of a nonstandard definition of "indirect."

- Consequently, this LLC is not a “corporation.”

- If this LLC is not a “corporation,” it cannot be a “reporting corporation.”

- Conclusion: a domestic LLC, if owned by a domestic corporation, does not file Form 5472.

Form 5472 is filed by "reporting corporations" only

IRC §6038A places the Form 5472 filing burden on "reporting corporations."

(a) Requirement. If, at any time during a taxable year, a corporation (hereinafter in this section referred to as the “reporting corporation”)—

(1) is a domestic corporation, and

(2) is 25-percent foreign-owned,

such corporation shall furnish, at such time and in such manner as the Secretary shall by regulations prescribe, the information described in subsection (b) and such corporation shall maintain (in the location, in the manner, and to the extent prescribed in regulations) such records as may be appropriate to determine the correct treatment of transactions with related parties as the Secretary shall by regulations prescribe (or shall cause another person to so maintain such records).

How do we know that Form 5472 is the required form?

Easy: Regs. §1.6038A-1(b) tells us:

(b) In general. A reporting corporation must furnish the information described in § 1.6038A-2 by filing an annual information return (Form 5472 or any successor), and must maintain records as described in § 1.6038A-3.

A “reporting corporation” is, of course, a corporation

The filing obligation is imposed on a corporation that is a "reporting corporation." The adjective (”reporting”) is bolted onto a noun (”corporation”) that has a well-known meaning in the Internal Revenue Code.

Sometimes, a disregarded entity is also a corporation

Confusingly, some entities can simultaneously be classified in two different ways for U.S. income tax purposes.

The situations where a disregarded entity is, for a special purpose, also classified as a corporation, are listed in Reg. §301.7701-2(c)(2)(i) through (vi).

Some disregarded entities are classified as corporations for Form 5472 purposes

The Regulation

Reg. §301.7701-2(c)(2)(vi)(A) says that some business entities that are classified as disregarded entities for all tax purposes will nevertheless be classified as corporations for purposes of complying with IRC §6038A (the Form 5472 statute). With emphasis added:

(A) In general. An entity that is disregarded as an entity separate from its owner for any purpose under this section is treated as an entity separate from its owner and classified as a corporation for purposes of section 6038A if -

(1) The entity is a domestic entity; and

(2) One foreign person has direct or indirect sole ownership of the entity.

In other words, for a domestic disregarded entity to be classified as a corporation for purposes of IRC §6038A, two things are necessary:

- It is the right kind of entity; and

- It has the right kind of foreign ownership.

The right kind of entity . . .

We have the right kind of entity. The Regulations require:

- a domestic entity [Reg. §301.7701-2(c)(2)(vi)(A)(1)]

- that is disregarded as an entity separate from its owner for any purpose [Reg. §301.7701-2(c)(2)(vi)(A)].

A domestic limited liability company with one owner satisfies that requirement. It is a domestic entity, and it is disregarded as an entity separate from its owner (the domestic corporation subsidiary).

The first of the two conditions is satisfied.

. . . and the right kind of foreign ownership

The second condition needed to make a disregarded entity be classified as a corporation for IRC §6038A purposes is the right kind of foreign ownership. The requirement is at Reg. §301.7701-2(c)(2)(vi)(A)(2):

(2) One foreign person has direct or indirect sole ownership of the entity.

This requires knowing the meaning of:

- “direct sole ownership,” and

- "indirect sole ownership."

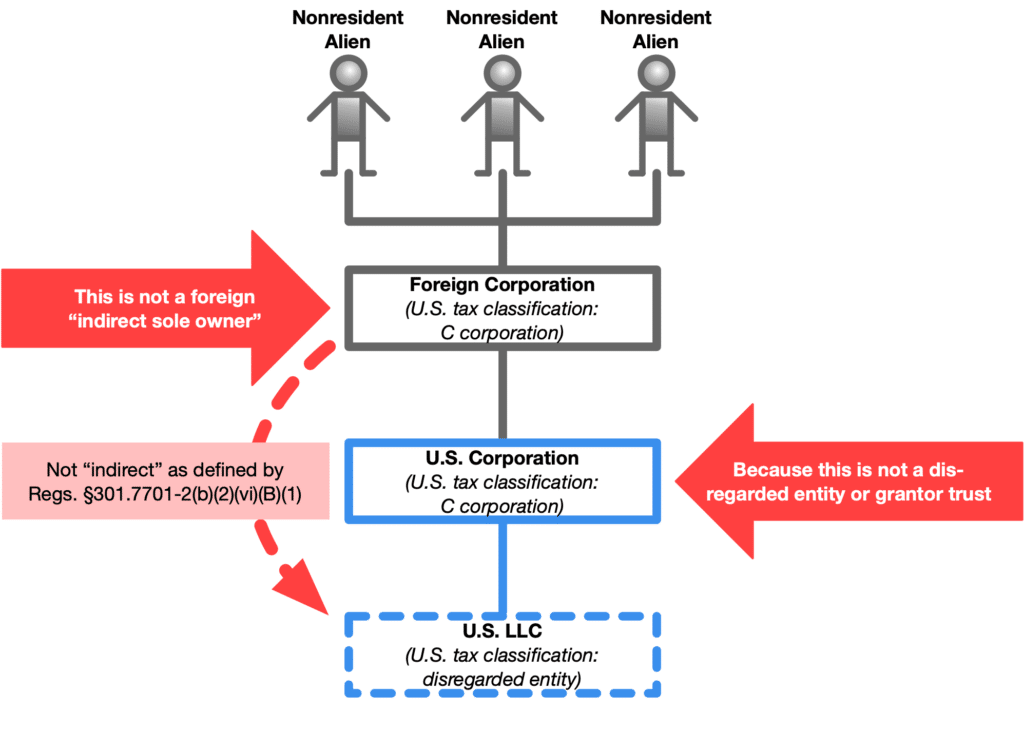

An LLC owned by a domestic corporation has the wrong kind of foreign “indirect” ownership

Direct sole ownership by a foreign person is self-evidently not true: the LLC is owned by a domestic corporation. The question to analyze is whether the LLC in our example has foreign “indirect sole ownership.”

A foreign person does not have "sole indirect ownership"

"Indirect sole ownership" means that when you look up from the domestic limited liability company in question, all the way up the ownership stack, you must see nothing but disregarded entities or grantor trusts until you reach one person (who happens to be foreign). No corporations, no trusts, no partnerships.

Reg. §301.7701-2(c)(vi)(B)(1) says it like this (emphasis added):

(1) Indirect sole ownership. For purposes of paragraph (c)(2)(vi)(A)(2) of this section, indirect sole ownership means ownership by one person entirely through one or more other entities disregarded as entities separate from their owners or through one or more grantor trusts, regardless of whether any such disregarded entity or grantor trust is domestic or foreign.

The domestic corporation subsidiary is not disregarded as an entity separate from its owner. It's a corporation.

Therefore, the foreign parent corporation cannot have "indirect sole ownership" of the domestic limited liability company (as that term is defined by Reg. §301.7701-2(c)(vi)(B)(1)) — because a corporation is in the holding structure, between the foreign corporation (the would-be "sole foreign owner") and the domestic limited liability company (the entity that we are testing to see whether it should be specially-classified as a corporation for Form 5472 purposes).

The second of the two conditions for treating the domestic limited liability company as a corporation has failed.

Consequently, this LLC is not a “corporation”

Just to quickly summarize the discussion, in order for a domestic disregarded entity to be classified as a corporation for IRC §6038A purposes, two things must be true. Only one of them is true in the fact pattern described above.

- Entity type: true. A domestic limited liability company is the right kind of disregarded entity for classification as a corporation for purposes of IRC §6038A.

- Ownership: false. However, the domestic limited liability company has the wrong kind of ownership. It does not have a direct foreign owner or an indirect foreign owner of its membership interests.

Therefore, in the example give above the domestic limited liability company is not a "corporation" for purposes of IRC §6038A.

If this LLC is not a “corporation,” it is also not a “reporting corporation”

A “reporting corporation” is defined as a domestic corporation [IRC §6038A(a)(1)] that has at least one foreign shareholder holding 25% or more of the stock of the corporation [IRC §6038A(a)(2)].

This limited liability company is not classified as a corporation for purposes of IRC §6038A(a) by the special rule in the Regulations.

Therefore, it cannot be classified as a domestic "corporation" as required by IRC §6038A(a)(1) and will therefore not be a "reporting corporation."

Conclusion: this LLC will not file Form 5472

Only “reporting corporations” have a Form 5472 filing requirement. This domestic limited liability company is not a “reporting corporation.”

Therefore, this domestic limited liability company cannot have a Form 5472 filing obligation.